Barclays

Summary

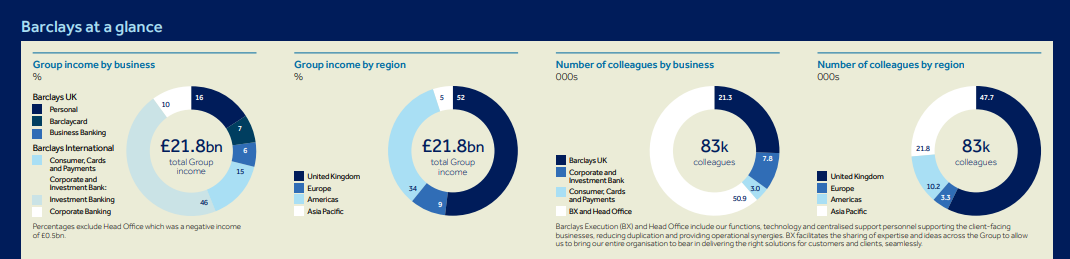

- Barclays operates as two divisions, Barclays UK and Barclays International, supported by the service company, Barclays Execution Services.

- Barclays UK (BUK) consists of UK Personal Banking, UK Business Banking and Barclaycard Consumer UK businesses.

- Barclays International (BI) consists of Corporate and Investment Bank and Consumer, Cards, and Payments businesses.

Company Overview

Barclays (NYSE:BCS, LSE:BARC) traces its ancestry back to two goldsmith bankers, John Freame and Thomas Gould, who were doing business in Lombard Street, London in 1690. In 1736, Freame’s son, Joseph took his brother-in-law, James Barclay on as a partner, and the name has remained a constant presence in the business ever since.

Barclays was built over centuries. The company's longevity is an extraordinary achievement, especially against the backdrop of multiple financial crises, international conflicts, and the agricultural, industrial, and now technological revolutions.1

Business Overview

Barclays operates as two divisions, Barclays UK and Barclays International, supported by its service company, Barclays Execution Services.2

Barclays UK

Barclays UK (BUK) consists of its UK Personal Banking, UK Business Banking and Barclaycard Consumer UK businesses. These businesses are carried on by its UK ring-fenced bank (Barclays Bank UK PLC) and certain other entities within the Group.

UK Personal Banking offers retail solutions to help customers with their day-to-day banking needs. UK Business Banking serves business clients, from high growth start-ups to SMEs, with specialist advice for their business banking needs. Barclaycard Consumer UK is a leading credit card provider, offering flexible borrowing and payment solutions, while delivering a leading customer experience.

Barclays International

Barclays International (BI) consists of its Corporate and Investment Bank and Consumer, Cards and Payments businesses. These businesses are carried on by its non-ring-fenced bank (Barclays Bank PLC) and its subsidiaries, as well as by certain other entities within the Group.

With relentless focus on delivering for customers and clients around the world, Barclays International’s diversified business portfolio provides balance, resilience and exciting growth opportunities. The division has strong global market positions and continues to invest in people and technology in order to deliver sustainable improved returns. Barclays International offers customers and clients a range of products and services spanning consumer and wholesale banking.

Barclays Execution Services

Barclays Execution Services (BX) is a Group-wide service company providing technology, operations, and functional services to businesses across the Group.

Financial Highlights

Barclays PLC H1 2022 Results

Attributable profit was £2.5bn (H121: £3.8bn) and RoTE was 10.1% (H121: 16.1%) having reflected a £0.6bn net of tax impact for the Over-issuance of Securities in the US (Over-issuance of Securities). Excluding this impact, RoTE was 12.5% 3

Barclays' diversified model delivered a profit before tax of £3,733m (H121: £4,902m), RoTE of 10.1% (H121: 16.1%), and earnings per share (EPS) of 14.8p (H121: 21.9p).

Total income increased to £13,204m (H121: £11,315m). Barclays UK income increased 5%. Barclays International income increased 21%, with CIB income up 21% and CC&P income up 20%. Excluding the income benefit of £758m from hedging arrangements related to the Over-issuance of Securities, total Group income was £12,446m, up 10% year on-year, Barclays International income was £9,182m, up 12% year-on-year and CIB income was £7,213m, up 10% year on-year.

Credit impairment charges were £341m (H121: £742m net release) reflecting low flows to delinquency and an improved UK employment outlook, partially offset by a day one charge relating to the acquisition of the GAP Inc. US credit card portfolio (the GAP portfolio). Expert judgement post-model adjustments have been maintained to incorporate customer affordability and inflationary headwinds.

Total operating expenses increased to £9,127m (H121: £7,308m). Operating costs increased 2% to £7,270m, reflecting continued investment and business growth, the impact of inflation and the appreciation of average USD against GBP, partially offset by efficiency savings and the non-recurrence of structural cost actions, primarily relating to the real estate review in June 2021.

The effective tax rate (ETR) was 22.0% (H121: 15.1%). The tax charge included a £346m charge recognised for the remeasurement of the Group’s UK deferred tax assets (DTAs) due to the enactment of legislation in Q122 which will result in the UK banking surcharge rate being reduced from 8% to 3% effective from 1 April 2023. The ETR excluding the impact of this downward re-measurement of UK DTAs was 12.8% which included a 5.8% benefit relating to adjustments in respect of prior years

Attributable profit was £2,475m (H121: £3,752m) including the net impact of the Over-issuance of Securities net of tax, of £581m, of which £341m was in Q222

Total assets increased to £1,589bn (December 2021: £1,384bn) primarily due to an increase in client and trading activity, and growth in the liquidity pool

TNAV per share increased to 297p (December 2021: 291p) primarily reflecting 14.8p of EPS, partially offset by net negative reserve movements driven by higher interest rates.

Barclays UK

Barclays UK delivered a RoTE of 17.0% (H121: 20.6%), and a lower cost: income ratio of 62% (H121: 67%), reflecting improved income performance across Personal Banking and Business Banking, alongside reduced total operating expenses, while impairment returned to a charge following a net release in H121. Barclays UK remains well positioned, with a strong focus on supporting customers in an increasingly difficult and uncertain environment.

Barclays International

Barclays International delivered a RoTE of 11.5% reflecting the benefits of being a diversified business. CIB delivered a RoTE of 11.9% reflecting a strong performance in FICC, partially offset by a decrease in Investment Banking fees, against a strong prior year comparative, and provisions for litigation and conduct. CC&P RoTE decreased to 8.5% as an increase in income was offset by a provision for higher customer remediation costs relating to a legacy loan portfolio and continued investment in the business.

References

- ^ https://home.barclays/who-we-are/our-history/

- ^ https://home.barclays/content/dam/home-barclays/documents/investor-relations/reports-and-events/annual-reports/2020/Barclays-PLC-Annual-Report-2020.pdf

- ^ https://home.barclays/content/dam/home-barclays/documents/investor-relations/ResultAnnouncements/HY2022/20220728-Barclays-PLC-Interim-2022-Results-Announcement.pdf