City Union Bank Ltd

Overview

The City Union Bank (NSE:CUB) was incorporated as a limited company on 31st October, 1904 carrying name 'The Kumbakonam Bank Limited'. The bank in the beginning preferred the role of a regional bank and slowly but steadily built for itself a place in the Delta District Thanjavur. The first Branch of the Bank was opened at Mannargudi on 24th January 1930. Thereafter, branches were opened at Nagapattinam, Sannanallur, Ayyampet, Tirukattupalli, Tiruvarur, Manapparai, Mayuram and Porayar within a span of twenty five years. The Bank was included in the Second Schedule of Reserve Bank of India Act, 1934, on 22nd March 1945.1

In 1957, the bank took over the assets and liabilities of the Common Wealth Bank Limited and in the process annexed to it the five Branches of Common Wealth Bank Limited at Aduthurai, Kodavasal, Valangaiman, Jayankondacholopuram and Ariyalur.

In April, 1965, two other local banks viz., 'The City Forward Bank Limited' and 'The Union Bank Limited' were amalgamated with the Bank under a scheme of amalgamation with the resultant addition of six more branches viz., Kumbakonam-Town, Nannilam, Koradacherry, Tiruvidaimarudur, Tirupanandal and Kuttalam. Consequently, the Bank's name was changed to 'The Kumbakonam City Union Bank Limited'.

The first branch outside the state of TamilNadu was opened at Sultanpet, Bangalore in Karnataka in September,1980. Branches were also opened at the twin cities of Hyderabad and Secunderabad in Andhrapradesh. In tune with the national image attached to the Bank, the Bank's name was changed to 'City Union Bank Limited' with effect from December, 1987.

Key Milestones

| Year | Event |

| 1904 | Incorporation of the Bank |

| 1945 | Scheduled bank since 22.03.1945 |

| 1957 | Took over CommonWealth Bank Limited |

| 1965 | Amalgamation of ‘TheCity Forward Bank Limited’ & ‘The Union Bank Limited’ with the Bank |

| 1998 | Initial Public Offering (IPO); Listing bank’sshares on the BSE, NSE & MSE |

| 2002 | Entered into agreement withTCS for core banking solution “Quartz” |

| 2003 | Obtained licenses to act as a agent for procuring insurance & general insurance business |

| 2007 | Preferential allotment for equity shares strengthening bank’s capital funds |

| 2009 | Rights Issue @ 1 : 4 - toreward the existing shareholders |

| 2012 | Rights Issue @ 1 : 4- to reward the existing shareholders & employees under “Employee Reservation Scheme |

| 2014 | Raised INR Rs.3,500 mn in Equity capital Through QIP route |

| 2017 & 2018 | Bonus Issue @ 1 : 10 - rewarded to the existing Shareholders |

As of Sep 2020 - 700 branches. 628 branches are located in South India out of which 485 in Tamil Nadu

| State | No. of Branches | % of Deposits | % of Advances | % of Business |

| Tamil Nadu | 485 | 80 | 64 | 72 |

| Karnataka | 41 | 6 | 6 | 6 |

| Andhra Pradesh | 45 | 3 | 8 | 5 |

| Telangana | 33 | 2 | 5 | 4 |

| Maharashtra | 20 | 2 | 3 | 3 |

| Kerala | 18 | 2 | 2 | 2 |

| Gujarat | 14 | 1 | 4 | 2 |

| Others | 44 | 4 | 8 | 6 |

| Total | 700 |

Industry Overview

The Indian economy performed well in the first half of FY2020 mainly due to various policy measures taken by the New Government at the Centre. India's GDP (Gross Domestic Product) grew at 5.2% in Q1, 4.4% in Q2, 4.1% in Q3 & 3.1 in Q4, aggregating to a growth of 4.2% for the full year. The slowdown in last quarter has been due to decline in economic activity because of the countrywide lockdown due to COVID19. With the economy hit by pandemic towards the end, the GDP for FY2020 would be below the government target of 5%. The retail inflation touched a high of 7.59% in month of January 2020 and declined thereafter to close at 5.81%. Crude Oil remained volatile with geopolitical events, supply-demand mismatches and resurgence of trade barriers. The Brent crude oil hovered between $74 / barrel and $20 / barrel in the year. The Agriculture sector however proved to be a silver lining, necessitated by sowing of pulses, rice and oilseeds in the summer months. Agriculture and Allied activities were buoyed by increase in Kharif and horticulture production. Domestic Air Traffic, Passenger and Commercial vehicle sales, Domestic Tourism, Hospitality & Trade experienced sizeable contraction. There has been a decline in private domestic consumption due to contraction of manufacturing activities. As per RBI reports, it is difficult to assess the depth of the damage caused by the pandemic and estimate how long will it take to return to normal levels. 2

The Indian Banking Sector which experienced mounting NPA's in FY 2018-19 started showing signs of revival in the first half of FY 2019-20. FY 2019 also saw a steady flow of Foreign Direct Investment of which the banking and financial sector received the highest share for the first three quarters of 2019-20. Public Sector Banks had also collectively posted net profits in the First Quarter of FY 2019-20 as against 2018-19. However, the Banking sector as of now is facing a tough task due to COVID-19 pandemic. The banking sector is likely to witness a partial recovery, following the revival of economy and gradual easing of lockdown. Fiscal measures by the government and significant Monetary and Liquidity measures by RBI would go a long way in mitigating the adverse impact on domestic economy and help boost economic activity once normalcy is restored.

The financial year turned favourable for the bond market with the Government Securities yields starting to fall from the high of 7.47% to 6.07% during the year. The first half of financial year saw yield falling with various positive factors like the continuation of government in centre, benign inflation etc. The yield also saw spikes due to increase in core inflation and concerns about fiscal deficit which was offset by RBI's Open market intervention.

During the financial year 2019-20, Indian Rupee weakened against USD by 9.4% and the major reason being US China trade war and Corona Virus outbreak. Indian Rupee against USD opened at `69.15 and closed at `75.66. The large FPI outflows towards the second half of FY aggravated the situation. Compared to other currencies, Indian Rupee performed better with RBI's intervention. The low crude oil prices kept the rupee from weakening further. With a healthy foreign exchange reserves, the Indian Rupee remained at a comfort zone against USD.

Financial Overview

Given the market conditions, the Bank recorded a moderate growth rate during the year. The credit growth remaining subdued during the year, the biggest challenge faced by the Banking system was dealing with stressed assets, restructured debts and NPA accounts. Despite these challenges, the Bank was able to post a 5% growth in its total business, with Deposits growing by 6% and Gross Advances growing by 5%. The total business of the Bank as on March 31, 2020 stood at Rs 75,408 crore.

The performance of the Bank during the financial year ended March 31, 2020 remained stable with a total income of Rs 4,848.55 crore as compared to Rs 4,281.55 crore during the previous year recording growth of 13% and Net Interest Income recorded a growth of 4% to Rs 1,675.19 crore from Rs 1,611.49 crore last year.

As on March 31, 2020, the Deposits of the Bank increased to Rs 40,832.49 crore as compared to Rs 38,447.95 crore as at March 31, 2019. Total CASA improved by 5% from Rs 9,698.19 crore last year to Rs 10,196.95 crore in FY 2019- 20. The proportion of CASA to total deposits was at 25% as on March 31, 2020. The cost of deposits stands slightly increased to 6.20% for FY 2020 against 6.17% as at March 31, 2019.

The Gross Advances of the Bank increased by Rs 1,510.92 crore to Rs 34,576.17 crore from Rs 33,065.25 crore, posting a growth of 5% coupled with a Net Interest Margin (NIM) of 3.98% for the year ended March 31, 2020. The yield on advances declined to 10.76% from 10.95% during the financial year due to transmission of policy rates and also stiff competition among banks. Other income earned for the financial year ended March 31, 2020 has improved significantly to Rs 679.95 crore from Rs 514.39 crore last year mainly on account of treasury income. The Return on Assets as on March 31, 2020 was 1% and for March 31, 2019, it was 1.64%.

As the credit growth was slightly sluggish during the year, the investment of the bank rose to Rs 9,236.25 crore against Rs 7,863.33 crore in FY 2019. The yield on 10 year benchmark closed at 6.14% in March 2020, amidst surging crude oil prices, CPI being higher than RBI target for several months. Despite positive triggers provided by Government of India, overall negative sentiments weighed on markets. Through the timely sale of securities, the Bank had booked a profit to the tune of Rs 159.60 crore as against Rs 32.56 crore during the previous year.

During FY 2020, operating expenses increased by 14% to Rs 1,013.74 crore from Rs 885.89 crore in FY 2019. The staff expenses increased from Rs 364.44 crore last year to Rs 420.65 crore in FY 20. During the year, the Bank had opened 50 new branches and increased the number of ATMs to 1,793 which resulted in higher infrastructure and staffing expenses. The other operating expenses increased from Rs 521.45 crore to Rs 593.09 crore which was due to normal increase in expenses like rent, telephones and repairs & maintenance etc. The Cost to Income ratio was at 43.04% for the year ended March 31, 2020 as against 41.67% in the previous year.

Thus, the Bank has recorded a growth of 8% in Operating Profit from Rs 1,239.99 crore in FY 2018-19 to Rs 1,341.40 crore in FY 2019-20. The operating profit to NII constitutes 80%. The total provisions for FY20 increased to Rs 865.08 crore from Rs 557.14 crore in FY19. Tax provision decreased to Rs 110 crore in FY 20 as against Rs 242 crore last year on account of reduction in tax rate. The provision for NPA had increased to Rs 631 crore in FY 2020 against Rs 270 crore in FY 2019 on account of increase in slippages. The Bank had also made COVID provision to the tune of Rs 102 crore over and above the regulatory requirement.

The Bank recorded a Net Profit of Rs 476.32 crore as on March 31, 2020.

Return on Assets of the Bank for the FY 2019-20 stands at 1% and Return on Equity was at 9.47. The basic earnings per share stood at Rs 6.48 per share as compared to Rs 9.57 per share last year. The book value per share of the Bank increased from Rs 65.91 to Rs 71.83 as on March 31, 2020 as compared to previous year.

Recent developments

City Union Bank September 2020 Net Interest Income (NII) at Rs 475.14 crore.3

Financial Performance Q2FY2021

Net Interest Income

The Bank earned a Net Interest Income of Rs475cr as against Rs412cr for the same period as compared to last year.

Non Interest Income

Non Interest Income of the Bank is at Rs169cr in Q2FY2021 as against Rs195cr for Q2FY 20. The income earned on CEB & Charges decreased by Rs11crs from Rs76cr in Q2FY 20 to Rs65cr in Q2FY21 based on the instructions from Finance Ministry wrt waiver of charges due to COVID impact in Q1 FY21. The treasury income reduced to Rs69cr in Q2FY21 Vs Rs79crs in Q2FY 20.

Operating Expenses

The operating expense for Q2FY21 is at Rs260cr and was same during the previous year. Establishment expenses increased from Rs113cr in Q2FY 20 to Rs120cr in Q2FY21 and all other operating expenses marginally decreased from Rs147cr to Rs140cr in Q2FY21.

Operating Profit

Thus, the Operating Profit for Q2FY2021 was Rs385cr as against Rs347cr for the same period as compared to the last year.

Provisions

The Bank already holds a provision of Rs225cr for Covid-19 as on June 30, 2020 and during the current quarter the Bank has made an additional provision of Rs115cr to meet any future contingency arising out of Covid pandemic. Thus, the total provision in this regard held by the bank as on 30th September 2020 is Rs340cr.

Net Profit

The Bank’s Profit after Tax was at Rs158cr in Q2FY2021 as against Rs194cr in Q2FY 2020. Profit Before Tax for the quarter was impacted on account of additional provision made to the tune of Rs115cr towards Covid to meet any future contingency.

Deposits

Total Deposits of the bank marginally increased by 2% for Q2FY2021 to Rs41,421cr from Rs40,451cr for the same period as compared to last year. City Union Bank has not pushed for growth because of covid and to protect the margins along with optimum level ofcredit deposit ratio, the deposit position was kept muted in H1 FY21. However, the company will push for growth if situation warrants by way of any surge in advances in the second half of FY21. CASA increased by 7% from Rs9,988cr to Rs10,645cr (Y-o-Y). CASA portion stood at 25.70% to total deposits. Cost of Deposits decreased to 5.54% from 6.25% in Q2FY 20.

Advances

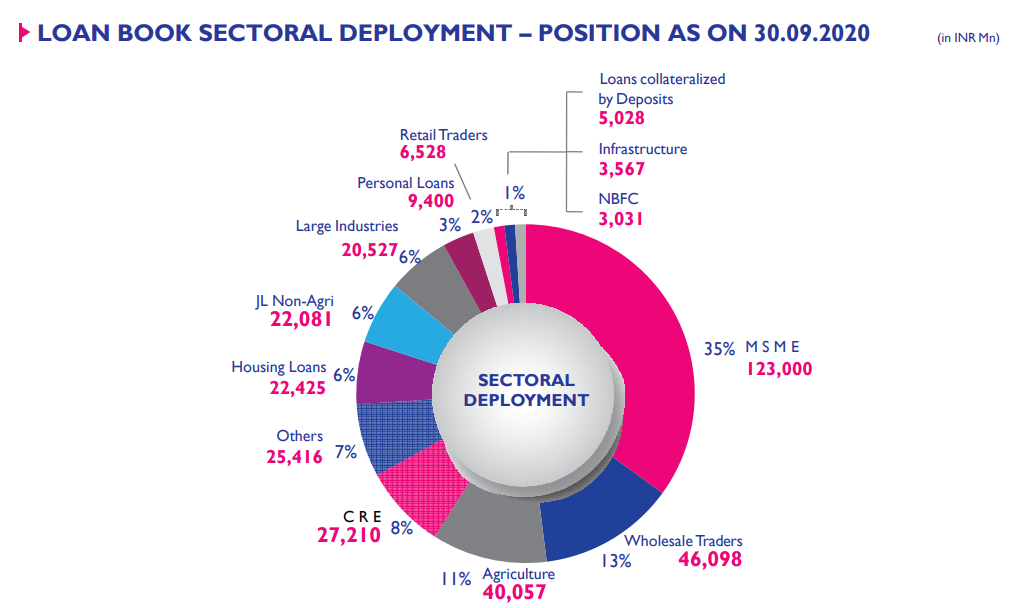

Total Advances increased by 6% for Q2FY2021 to Rs35,437cr from Rs33,279cr in Q2FY 2020.credit Deposit ratio stood at 86%. The yield on Advances decreased to 10.21% in Q2FY21 from 10.76% in Q2FY 20.

Asset Quality

The Gross NPA as on September 30, 2020 was at 3.44% and Net NPA was at 1.81% (Gross NPA as on June 30, 2020 was at 3.90% and Net NPA was at 2.11%). The Provision Coverage Ratio as on September, 2020 was at 70%. No addition to NPA during Q2FY21 because of standstill clause as per the direction of Supreme Court. Due to that Net NPA stands reduced to 1.81% in Sep-20 from 2.29% in Mar-20.

Net Interest Margin

Net Interest Margin stood at 4.12% in Q2FY21 Vs 3.91% in Q2FY20. NIM has increased sequentially from 3.98% in Q1FY21 to 4.12% in Q2FY21.

Capital Adequacy

As on September 30, 2020 the Capital Adequacy Ratio increased to 17.36% (With Tier I 16.29% and Tier II 1.07% as per Basel III norms). RWA reduced from Rs32,462cr in Mar-20 to Rs30,912cr in Sep-20 mainly due to sanction of ECLGS & increase in Gold loans during H1 FY21.

Return on Assets

Return on assets for the quarter is 1.23% as against 1.62% for the same period of last year.

Return on Equity

Return on Equity was at 11.50% in Q2FY2021 as compared to 15.18% in Q2FY2020.

Cost Income Ratio

Cost to Income Ratio reduced to 40.31% in Q2FY2021 from 42.87% in Q2FY 2020. The reduction was on account of improvement in Net Interest Income.

Moratorium

The Bank has extended the option to all the borrowers to avail moratorium as per the RBI instructions. During June quarter accounts covering an exposure of 1.76% of CC & 26.54% of Term loan, on total 12.45% of exposure did not received even single payment utilizing moratorium fully. That number currently stands at 0.65% of CC exposure, 19.12% of Term loan exposure and 9.03% of total exposure, where not even a single payment received during moratorium period. Out of them, 0.10% of cc exposure, 10.76% term loan exposure & 4.94% of total exposure have paid the demand portion of one monthly installment in the month of September 2020. Of the balance 4.09% of exposure have not paid anything till now, the company expect many of them would opt for restructuring since the time is available upto 31.12.2020 for NonMSME and 31.03.2021 for MSME.

ECLGS

Across business lines, upto October 2020, the Bank has sanctioned Rs1967cr and disbursed Rs1,691crs under the ECLGS.

Restructure

In terms of RBI Circular DOR No.BP.BC.34/21.04.048/2019-20 dt 11.02.2020 and DOR.No.BP.BC/4/21.04.048/2020-21 dated 06.08.2020 - Restructuring of Advances, the bank has restructured 11 Standard accounts to the tune of Rs79cr in Q2FY2021. As of H1 FY21, the total outstanding restructured Standard accounts was 175 in numbers and amounting to Rs478cr. The Bank hold a provision of Rs14cr against the requirement of Rs13cr towards Restructured Standard accounts.