Glencore

Summary

- Glencore is one of the world’s largest globally diversified natural resource companies.

- Founded in the 1970s as a trading company, Glencore become a major producer and marketer of commodities - employing 135,000 people.

- Glencore one of the world’s largest producers and marketers of copper.

Company Overview

Glencore (NYSE:GLEN, LSE:GLEN) is one of the world’s largest globally diversified natural resource companies.1

Founded in the 1970s as a trading company, Glencore now a major producer and marketer of commodities - employing 135,000 people around the world.

The company's operations comprise around 150 mining, metallurgical and oil production assets.

Recent Developments

Sale of BaseCore Metals LP2

12 July 2022; Glencore today announces the completion of the sale of a royalty package by BaseCore Metals LP ("BaseCore") to Sandstorm Gold Ltd. (“Sandstorm”) for total consideration of US$525 million. BaseCore is owned 50:50 by Glencore and Ontario Teachers’ Pension Plan Board (“OTPP”).

Total transaction consideration was comprised of US$425 million in cash and US$100 million in common shares of Sandstorm as of the announcement date, representing an ownership interest in Sandstorm of 5%.

BaseCore was created in 2017 as a joint venture limited partnership focused on base metals streams and royalties. Glencore contributed a portfolio of selected royalties, which were valued at US$300 million at the inception of the partnership with OTPP.

Glencore expects to receive approximately $300 million in cash and Sandstorm shares for its 50% interest in BaseCore, including retained cash on balance sheet that will be distributed to Glencore after which the intention is to collapse the business.

Financial Highlights

Group net income attributable to equity holders improved from a loss of $1,903 million in 2020 to an income of $4,974 million in 2021, after recognising various significant items discussed below. EPS increased from negative $0.14 per share to positive $0.38 per share.

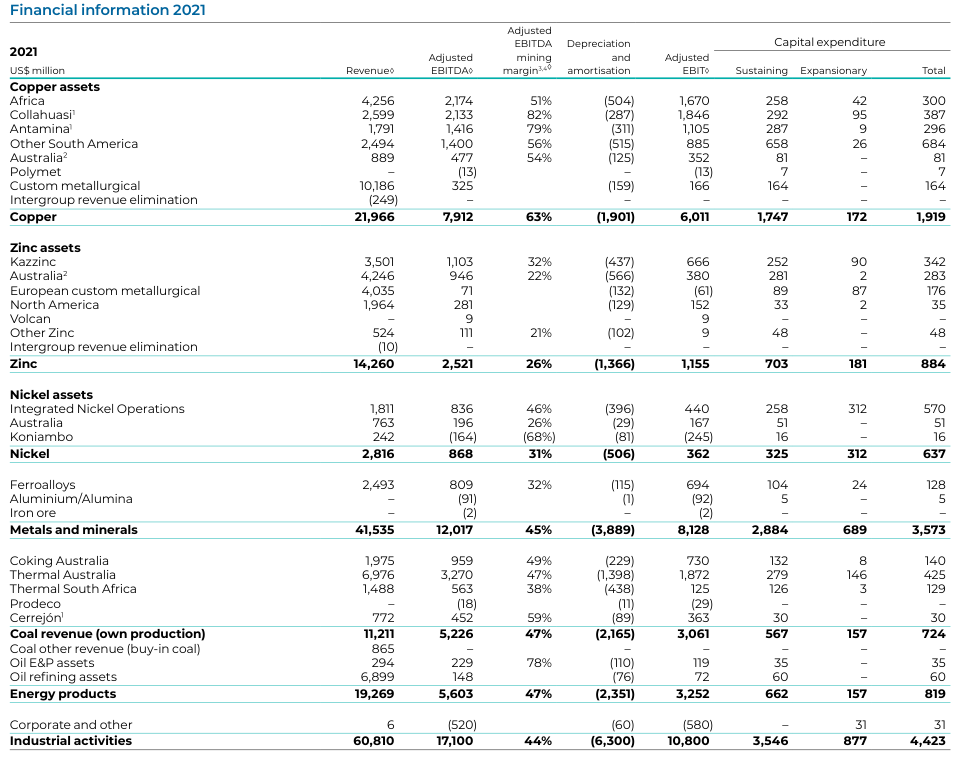

The economic recovery seen in late 2020 continued into 2021, helped significantly by major governments and central banks initiating and sustaining the provision of material stimulus to the global economy. Average year-over-year price increases for coal (Newc), cobalt, copper, nickel and zinc were 125%, 60%, 51%, 34% and 32% respectively. Owing mainly to such higher prices, Adjusted EBITDA set a record of $21,323 million and Adjusted EBIT was $14,495 million in 2021, compared to $11,560 million and $4,416 million in 2020. The positive impact of the higher commodity prices on Adjusted EBITDA was somewhat tempered by higher costs (mainly energy), the effects of a weaker US dollar against most of its producer currencies, including average year-over-year declines against the Australian dollar (9%) and the South African rand (10%) and modestly lower production levels. Adjusted EBITDA mining margins improved to 45% (2020: 36%) in its metal operations and to 47% (2020: 17%) in its energy operations.

Industrial Adjusted EBITDA increased by 118% to $17,100 million (Adjusted EBIT was $10,800 million, compared to $1,077 million in 2020). As noted above, the increase was primarily driven by stronger average year-over-year commodity prices, particularly related to its copper, cobalt, ferrochrome, nickel and coal operations, driven by recovery of global demand and various supply challenges, most notably seen across the energy spectrum (gas, coal and oil), impacting product availability and cost.

Net finance costs were $1,140 million during 2021, a 22% decrease compared to $1,453 million in the comparable reporting period, due to lower average base rates (mainly US$ Libor) and lower net funding levels year-over- year. Interest expense for 2021 was $1,348 million, down 14% over 2020 and interest income was $208 million compared to $120 million in the prior year.

An income tax expense of $3,026 million was recognised during 2021, compared to a credit of $1,170 million in 2020. The effective tax rate is 63.6%, and when adjusting for significant items (primarily impairments, foreign exchange adjustments and tax losses not recognised), the effective tax rate reduces to 33.5% (29.7% in 2020).

Net funding as at 31 December 2021 decreased by $4.6 billion to $30,837 million and net debt (net funding less readily marketable inventories) decreased by $9.8 billion to $6,042 million, as funds from operations of $17,057 million significantly exceeded the $3,802 million of net capital expenditure and $3,024 million of distribution to shareholders, non-controlling interests and purchase of own shares.

Operations

Metals and Minerals

The company produce and market a diverse range of metals and minerals – such as copper, cobalt, zinc, nickel and ferroalloys - and also market aluminium/alumina and iron ore from third parties.3

Copper

Glencore is one of the world’s largest producers and marketers of copper. In 2020, the company produced 1.26 million tonnes, and sold 3.4 million tonnes through its marketing business.

The company mine and process copper ore in the key mining regions of Africa, Australia and South America. The company source and recycle copper scrap in North America and Asia. And the company smelt and refine copper at smelters and refineries.

The company's copper marketing business supplies to customers in the automotive, electronics and construction industries.

As a major by-product of copper production, Glencore is one of the world’s largest producers of cobalt, primarily from the Democratic Republic of Congo (DRC).

The company's copper assets range from mines to smelters, refineries and recycling plants.

Cobalt

Glencore is one of the world’s leading producers of cobalt – a metal in rising demand thanks to its use in batteries for electric vehicles and portable electronics.

The company produce cobalt mainly as a by-product of copper mining in the Democratic Republic of Congo (DRC), but also as a by-product of nickel mining in Australia and Canada.

Glencore is also one of the largest recyclers and processors of cobalt-bearing materials, such as used batteries – helping secure the supply of the metal at a time of increasing demand.

Cobalt is mainly produced as a by-product at assets that produce copper or nickel.

Nickel

Glencore is a leading producer and marketer of nickel, with assets in Australia, Canada and Europe.

Zinc and Lead

The company mine and process zinc and lead ores in the key mining regions of Australia, South America, Kazakhstan and Canada. And, the company smelt and refine zinc and lead at processing operations in Australia, Canada, Spain, Italy, Germany, the UK and Kazakhstan.

The company also source and recycle zinc and lead materials in Europe and North America.

Through its marketing activities, the company sell zinc and lead concentrates; zinc and lead metals produced from concentrates; and valuable by-products such as sulphuric acid.

The company also sell gold and silver, which are typically mined together with zinc and lead ores.

The company market zinc and lead not only from its own facilities, but also from third-party producers.

The company's combination of mines and smelters means the company can produce, process and market zinc and lead across the world.

Ferroalloys

The company produce and market chrome ore, ferrochrome and vanadium, and Glencore is one of the world's largest and lowest-cost producers. The company also market manganese ore and alloys.

The company's chromite assets are held via its majority stake in the Glencore–Merafe Chrome Venture, and its vanadium assets via its majority shareholding stake in the Rhovan-Bakwena Vanadium Venture.

Other metals and minerals

Glencore is a leading supplier in the global alumina and aluminium market – and also market iron ore.

Aluminium / alumina

The company process and sell products from a range of third-party aluminium and alumina producers.

These products include bauxite, which is the world’s main aluminium ore; alumina (an oxide derived from the processed ore); primary aluminium; and aluminium alloys.

Iron ore

The company physically market iron ore from third-party producers to customers – with Asia making up most of its customer base.

Energy

Glencore is a major producer and marketer of coal, with mines in Australia, Africa and South America – while its oil business is one of the leading marketers of crude oil, refined products and natural gas.4

Coal

Glencore is one of the world's largest producers and exporters of seaborne traded thermal and coking coal.

Coal is an important part of its global commodity portfolio and Glencore is focused on running a profitable business in a safe, efficient, responsible and sustainable manner.

The company's coal is used in power generation, steel making and industrial processes including the manufacturing of cement, aluminium and nickel.

About 85% of the coal the company produce is exported, the majority of it to countries where coal continues to play a leading role in power generation given its reliability and affordability. The remainder of the coal the company produce is used in domestic power generation in Australia and South Africa.

The company complement its own production with agency third party and traded volumes to help ensure its customers get the quantities and qualities of coal they require in a secure, reliable and timely manner.

The company operate 26 mines in 21 mining complexes across Australia, Colombia and South Africa, supported by marketing offices across 19 countries.

Oil

Glencore is one of the world’s leading marketers of crude oil and oil products, supplying millions of barrels of oil every day.

The company source crude oil and oil products from a range of suppliers – through its marketing offices in London, New York and Singapore.

To support its business, Glencore has a substantial shipping portfolio and access to a range of logistics, storage and investment capabilities.

The company also market natural gas, mostly in Europe.

Through Astron Energy, Glencore is a leading supplier of petroleum products in South Africa, with a vast network of Caltex-branded service stations that make it one of the country’s top two petroleum brands. Astron also owns and operates the country’s third-largest crude oil refinery in Cape Town, which has a capacity of 100,000 barrels a day, and a lubricants manufacturing plant in Durban.

Marketing

Glencore is one of the world’s leading marketers of physical commodities.5

The company physically source commodities and products from its global supplier base – and sell them to customers all over the world.

This means transporting commodities by sea, rail and truck, storing them, processing them, and delivering them to the time, quality and specification that its customers need.

Through these marketing activities, the company set itself apart from companies who focus mainly on commodity production.

Recycling

Glencore is a market leader in the recycling of copper and precious metals.6

Glencore Recycling is a market leader in the recycling of copper and precious metals, committed to producing the commodities the world needs to advance everyday life. Glencore has more than 70 years’ experience in the recycling industry and operate a fully integrated business.

The company's network of marketing offices, sampling facilities on both coasts of the United States, copper, lead and nickel metallurgical operations in Canada, and broad customer base, make it one of the world’s leading copper and precious metals recycling companies. The company receive a wide range of materials from over 30 countries. Approximately 15% of the raw material feed for its smelting operations in Canada is from recyclable materials.

The company recycle a wide variety of complex end-of-life electronics in order to extract sustainable copper and precious metals, helping support a circular supply chain that gives a second life to products that might otherwise be sent to landfill.

Electronics

The company process a diverse range of end-of-life electronics, such as circuit boards, electronic components (e.g. connectors, pins, integrated circuits), cell phones, and insulated copper wire.

Copper bearing materials

The company recycle a wide range of copper bearing scrap, such as, high grade copper ( Cu), brass, turnings, and residues (dross, muds, hydroxide, dust and catalysts)

Precious metal bearing material

The company recycle various precious metal bearing materials, such as autoshred fines, IBAs, metallics, plated copper and filter cake.

Industry Overview

Commodity markets generally performed well throughout the year, bolstered by a widespread economic recovery, following the pandemic’s severe economic impacts in 2020, characterised by the imposition of lengthy lockdowns.7

Copper

Starting the year below $8,000/t, copper prices set a record high of $10,748/t in May, basis improved physical demand conditions, continued financial stimulus and high speculative positioning. Cathode premiums moved to their highest levels in five years, while LME cash copper traded at a premium to the three-month price, with a difference of over $1,000/t in October. During 2021, net imports of refined copper to the USA were at levels not seen in more than 10 years.

Looking forward, the company expect mine supply growth to be constrained by ageing assets, declining ore grades, a diminished project pipeline and the measures taken to contain the spread of Covid-19, with various new projects likely to experience delays. In the near term, the company expect global demand to remain strong, with steady growth rates longer term, driven by population growth and rising living standards in emerging economies. Climate change policies will also be a key driver for copper growth sectors, given its crucial role in accelerating the clean energy transition, from renewable power generation and distribution, to energy storage and electric vehicles (EVs).

Cobalt

2021 started strongly from a demand and pricing perspective, with positive momentum in Chinese and European EV demand and a level of stockpiling key strategic materials, particularly in China.

Commencing 2021 at $15.30/lb, prices rallied 65% through Q1 to reach a H1 high of $25.30/lb. Prices then cooled off somewhat before a strong recovery in H2 saw the year-end price at $33.50/lb. While the EV sector has been the main demand catalyst for cobalt, a number of metal demand segments exhibited post- Covid recovery.

Various cobalt supply projects are due to commission over the coming years, however elevated execution risk is likely to temper the rate at which new cobalt units are available, while incumbent production may also be impacted by continued logistical challenges. As a result, the cobalt market fundamental outlook remains robust.

Zinc

The zinc market recorded a deficit in 2021, driven by strong recovery in global demand (+6%), combined with production disruptions and supply chain bottlenecks. Average zinc prices increased 32% from $2,269/t in 2020 to $3,005/t in 2021, closing the year at around $3,600/t. Metal premiums were particularly strong outside China (Q4 2021: USA >$300/mt and EU c.$250/mt). At the same time, China required a significant amount of metal, with China’s State Reserves Bureau (SRB) releasing 180kt in 2021.

Looking ahead into 2022, refined zinc consumption is expected to increase, albeit not matching the percentage increase in 2021. There are risks to demand, including any Chinese construction slowdown and/or power-related demand destruction in Europe, however, there is upside from the potential comeback of the automotive sector as semiconductor shortages recede. Bottlenecks in logistics are expected to continue in the short and medium-term, creating regional differences.

Nickel

Primary nickel consumption rebounded sharply in 2021 (+17.5%), driven by record levels of stainless steel production in China and Indonesia and accelerating growth in the battery sector. The nickel market was in a substantial deficit in H1 2021, which narrowed in H2 as Indonesian nickel production continued to ramp up. Nickel stocks in LME warehouses fell by 60% in 2021.

EV sales grew strongly, despite a global slowdown in total automotive sales amid a shortage of parts and semiconductors. Automakers have broadly committed to electric mobility and are actively sourcing battery cells and raw materials. Stringent ESG requirements throughout the EV supply chain have resulted in a preference for high-grade nickel with a low carbon footprint.

Ferroalloys

Ferrochrome supply from South Africa, India and Europe recovered to pre-pandemic levels, resulting in global production growth of 15% year-on-year. This supply growth was met by a strong increase in global stainless steel melt rates, with Indonesian stainless steel production increasing by 87% year-on-year to 5mt, becoming the world’s second largest producer.

Vanadium demand recovered to pre- pandemic levels with stronger carbon steel markets absorbing excess inventory. The aerospace demand sector remained weak as previously noted.

Iron ore

Iron ore prices were extremely volatile throughout the year, driven by shifting policy initiatives and supply/demand rebalancing. Global resumption of construction activities and Chinese mills’ post winter restocking saw strong demand in H1 2021, supported by positive steel margins, with iron ore prices reaching 10-year highs in June. Chinese steel production cuts, instituted in large part to achieve annual environmental goals, led to a demand decrease in H2 while seaborne supply improved. Iron ore quickly became over-supplied, resulting in a significant price correction.

Aluminium

The aluminium market continued its strong recovery from the initial Covid-19 shock, backed by strong fundamentals, including a supply deficit. The price environment was volatile, as a surge in demand during H1 2021 was followed by rising energy costs first in China (Q2-Q3 2021) and then Europe during Q4 2021. Chinese imports of primary aluminium reached record levels, leading to a price rise on the LME, peaking at a decade- high of $3,229/t in mid-October. Prices retreated after China’s timely and effective coal reform, with the rally resuming towards year-end, mainly due to the European power crisis and subsequent smelter shutdowns.

Supported by physical tightness, Chinese imports and high logistics costs, premiums across the Americas, Asia and Europe increased significantly during 2021. The Midwest premium rose to an all-time-high of 35.4c/lb, ending the year at 30c/lb, while the Main Japanese Port premium finished the year at $170/t, up from $125/t at the beginning of the year.

The global bauxite market continued to be well-supplied. The military coup in Guinea in September raised concerns around supply- side risks, but these had largely eased by the end of the year, given alternative sources of supply.

Coal

Global seaborne thermal coal demand rose by c.43mt (5%) during 2021. Chinese seaborne demand increased by 64mt with supply from Australia falling from 31mt to zero as Australian coal restrictions persisted. The bulk of the 95mt swing in trade flows to China was supplied by Indonesia (+71mt) and Russia (+15mt). High gas prices supported increased thermal coal demand in Europe (+11mt), Korea (+5mt) and Taiwan (+4mt).

2021 saw record high average thermal coal prices for gCNewc ($137) and API4 ($125). API2 averaged $120/t, marginally below 2011. Coal prices peaked during October which was also a high point for LNG, as consumers looked to restock ahead of the winter period. GCNewc, API4 and API2 monthly prices peaked at 258%, 232% and 341% respectively above January’s price levels, before closing the year at $170/t (198%), $136/t (150%) and $137/t (202%) respectively.

Forward gas prices are at relatively high levels, with thermal coal remaining the lowest cost baseload fuel for power generation in all major seaborne markets. Weather-related supply impacts in Australia during December 2021 resulted in production and export shortfalls, which together with Indonesia’s temporary ban on coal exports, substantially limited spot coal availability in early 2022.

Oil

2021 marked another year of elevated volatility as the recovery from Covid-19 drove strong underlying demand growth for oil and gas. Prices were further supported by favourable financial markets and fiscal conditions. Further outbreaks of Covid-19 related strains in Q3 (Delta) and in Q4 (Omicron) threatened the trajectory of oil demand recovery, however such concerns proved short-lived, with Brent closing the year at $78 per barrel. The rising oil price through the year also prompted some releases of strategic petroleum reserves, led by the USA. This was absorbed by the market and did little to halt the price trajectory.

Refining margins in all regions continued to improve during 2021, largely driven by the recovery in transportation fuel markets as mobility restrictions eased and refined product inventories needed to be restocked. Other factors were Hurricane Ida disrupting refining operations in the US, elevated natural gas input costs in H2 2021 and China curbing oil product exports as part of its reforms to reduce carbon emissions and protect domestic supplies.

In shipping, tanker freight markets remained depressed for most of the year. Whilst they lifted in Q4, particularly in the ‘clean’ refined products segment, market expectations of a year-end upward momentum failed to materialise.

Company History

Glencore was founded in 1974. Today, Glencore is one of the world’s leading diversified natural resource companies, producing and trading more than 90 commodities.8

| Year | Milestones |

| 1974 | Glencore was founded in 1974. |

| 1974 | Marc Rich + Co AG is established, initially focusing on the marketing of ferrous and non-ferrous metals and minerals and crude oil. |

| 1981 | Granaria, a Dutch grain trading company acquired, which later becomes Glencore Agriculture. |

| 1987 | US smelter and Peruvian mine acquired; vertically integrated production starts. |

1990 | A stake in Xstrata (then Südelektra Holding AG) is acquired. |

| 1993 | Management buyout from Marc Rich; with the company being renamed Glencore. |

| 1995 | The company acquire the Prodeco coal project in Colombia – today, Colombia’s third largest exporter of thermal coal. |

| 2000 | The company acquire a stake in Mopani, Zambia – one of the African Copperbelt’s key producers of copper. |

| 2002 | The Xstrata IPO takes place in London. |

| 2008 | Katanga and Nikanor merger completes in the DRC. |

| 2012 | The company acquire Viterra – providing a significant operational footprint for its agriculture business in Australia and Canada. |

| 2013 | The company complete the merger with Xstrata. |

| 2013 | The company roll out the Code of Conduct across the Glencore group. |

| 2013 | The $550m Puerto Nuevo is opened in Colombia – one of Colombia’s first direct loading ports. |

| 2014 | The company become a member of ICMM – the International Council on Mining and Metals. |

| 2014 | Mopani Copper Mines $500m smelter upgrade completed. |

| 2016 | The company agree to sell 40% of Glencore Agricultural Products to CPPIB, and 9.9% to the British Columbia Investment Management Corporation. |

| 2017 | The company take full ownership of Mutanda and increase its stake in Katanga in the DRC. |

| 2017 | The company announce a joint venture with G500 in Mexico to launch 2,000 G500-branded gas stations. |

| 2017 | The company agree to acquire a 49% interest in Hunter Valley Operations. |

| 2017 | The company announce a deal to acquire Chevron’s South African and Botswanan mid/downstream assets. |

| 2017 | Glencore acquires 36.9% of the voting shares in the Peruvian zinc, lead and silver producer, Volcan. |

| 2018 | The company acquire the Hail Creek coal mine – a large-scale, long-life and low cost operation located in central Queensland, Australia. |

References

- ^ https://www.glencore.com/who-we-are/at-a-glance

- ^ https://www.glencore.com/media-and-insights/news/sale-of-basecore-metals-lp

- ^ https://www.glencore.com/what-we-do/metals-and-minerals

- ^ https://www.glencore.com/what-we-do/energy

- ^ https://www.glencore.com/what-we-do/marketing

- ^ https://www.glencore.com/what-we-do/recycling

- ^ https://www.glencore.com/.rest/api/v1/documents/ce4fec31fc81d6049d076b15db35d45d/GLEN-2021-annual-report-.pdf

- ^ https://www.glencore.com/who-we-are/our-history