Kotak Mahindra Bank Ltd

Company Overview

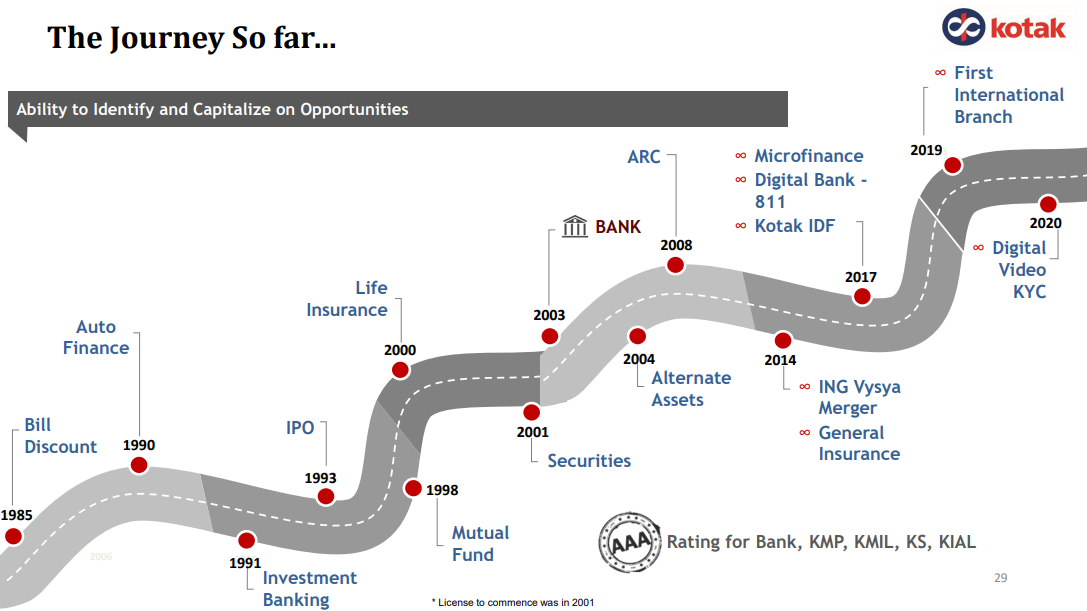

The Kotak Group has been in business for 35 years, and Kotak Mahindra Bank (NSE: KOTAKBANK) for 17 years now. The financial services of the Bank have a wide reach across 1,600 branches in India. Kotak also has a presence in Singapore, London, the USA and the Middle East through its international arms. All Group entities constantly endeavour to seize new opportunities by differentiating across products, services and technologies. Globally, Kotak serves the multiple financial services needs – banking (consumer, commercial, corporate), credit and financing, equity broking, wealth and asset management, insurance (general and life), and investment banking – of individuals and corporations.

video-based KYC savings account that serves the twin purpose of convenience and contactless opening of an 811 account in a highly digitised postCOVID ‘new normal’. The Bank’s reach is now extended beyond just its network, to a point where anyone in India can open a bank account from the safety and convenience of their houses. Kotak 811 launches India's first zero-contact, video KYC savings account.

Product Portfolio

Wholesale Banking

- Corporate Loans

- Trade Finance

- Business Banking

- Commercial Real Estate

- Forex/ Treasury

- Cash Management

- Custody Business

- Off-shore Lending

Commercial Banking

- Agriculture Finance

- Tractor Finance

- Commercial Vehicles

- Construction Equipment

- Microfinance

Consumer Banking

- Branch Banking

- 811

- Home loans, LAP

- Personal Loans

- Consumer Durable Finance

- Credit Cards

- Priority Banking

- Small Business Loans

- Private Banking

- Gold Loans

- Rural Housing & Business Loans

- Forex Cards

Other Financial Services

- Wealth Management

- Car and 2W Loans

- Mutual Funds

- Alternate Assets

- Off-shore Funds

- Life Insurance

- General Insurance

- Investment Banking / DCM

- Broking

- Loan against Shares

- Infra Debt Finance

- Asset Reconstruction

Business Overview

The company organize its principal banking business activities into the following business units: consumer banking, commercial banking, corporate banking, treasury, and other financial services. The consumer, commercial and corporate banking businesses correspond to the key customer segments of its Bank. The treasury offers specialized products and services to these customer segments and also undertakes asset liability management as well as proprietary trading for the Bank. 1

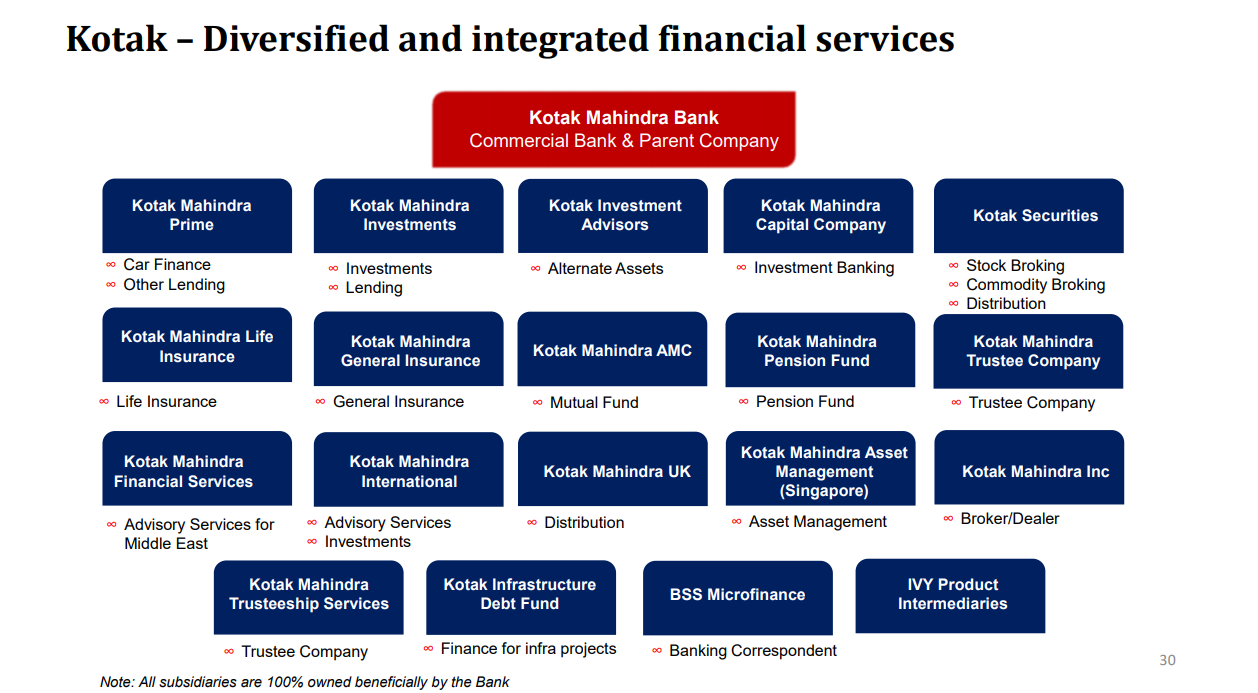

In addition to its banking activities, its Group offers a significant array of other financial products and services as well, which the company operate through its subsidiaries. These products and services include banking, financing through NBFCs, asset management, insurance, broking, investment banking, wealth management and asset reconstruction.

Consumer Banking

The Consumer Bank services a customer base in excess of 19 million customers covering a wide spectrum across domestic individuals and households, non-residents, small and medium business segments for a range of products from basic savings & current accounts to term deposits, credit cards, unsecured and secured loans, working capital and investment advisory.

The Bank continued its strategy of calibrated expansion of its branch network. As of 31st March, 2020, the Bank had 1,600 branches and 2,637 ATMs, covering 779 locations. Of the 100 new branches commissioned this year, 50 were in metro, 18 were in urban, 3 semi urban & 29 rural branches. Aided partly by 811, the Bank saw fast-paced customer acquisition across all core banking products including savings and current accounts, term deposits, overdrafts and non-resident accounts. The Bank has also set up 82 e-lobbies, and relocated 20 branches across metro and semi urban locations to give easier access and higher convenience to its customers.

The Bank rolled out several initiatives aimed at offering a superior and differentiated customer experience. The Bank’s investment in the phone based remote engagement through VRM (Virtual Relationship Model) yielded good results and the Bank has expanded this model to now serve over 0.8 million customers (across 10 languages) and provide them services across banking, deposit, lending and investment needs.

The Bank has continued to take significant steps in the area of digital initiatives.

The Bank continued to ramp up 811 acquisition numbers this year. The Bank also increased its focus on cross selling to these customers using newer digital channel like Whatsapp & Web Notifications, while also driving Digital channel adoption & transactions to better engage with existing 811 customers.

Additionally, after the new regulations on Aadhaar-based account opening in October 2019, the Bank has quickly enabled its officers to acquire new customers using Aadhaar-based biometric acquisition. Now on a monthly basis, 30% of the customers (non 811) are acquired digitally using Biometric authentication.

The Bank, in the last quarter of Financial Year 2020, launched an exclusive Salary Account offering for PSU and Government bodies. This offering comes with exclusive features like Permanent & Partial Disability Cover and Education benefit. With this offering, the Bank intends to foray into this large salaried segment to increase its mark on salary business.

For its premium Salary offering, the Bank tied up with vHealth by Aetna (Indian Health Organization) and offered Family Health Care Benefits, like free Health Check-up, unlimited Tele-consultation with doctors and discounts on various Health care benefits.

In line with the Bank’s overall strategy, the Non-Resident Indian Business has focused on enhancing customer experience through use of technology, across its banking products and platforms. As part of this endeavour, the Bank has gone live with 5 partners on Ripple, a distributed ledger based payment network facilitating seamless cross-border transactions. Additionally, the Bank on-boarded 11 new MSB (Money-transfer Service Business) relationships in the Financial Year 2019-20 to increase coverage across US, UK, Europe and Middle East.

In the Retail Institutional Business, the Bank introduced a collection solution-based UPI & Quick Response (QR) code, so as to digitise payments for traditionally cash-based segments like religious institutions. This solution solves collection-related requirement of clients and shall help the Bank to acquire new customers in this segment.

The Bank has actively taken part in various Financial Inclusion initiatives. The Bank has partnered with multiple Corporate Business Correspondents, and operates with more than 300 customer service points across Chhattisgarh, Karnataka, Tamil Nadu, Andhra Pradesh & Telangana, offering banking services and Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) payments to Beneficiaries. To enhance its reach and to build customer convenience, the Bank has successfully set up 145 Aadhaar Enrolment Centres in its branch premises and surpassed the transaction volume mandated by Unique Identification Authority of India (UIDAI). As a result of these efforts, the Bank has been recognized by UIDAI as the Best Performing Private Bank for conducting highest average daily transactions. The Bank has been awarded, twice, by the Pension Fund Regulatory Authority of India (PFRDA) as the Best Performing Private Sector Bank for highest persistency of Atal Pension Yojana (APY) subscribers.

Commercial Banking

The Bank’s Commercial Banking business focuses on meeting the banking and financial needs of various customer segments with deeper coverage that goes beyond metro and urban centers, through an expanding network of branches and associates. The business has specialized units which offer financial solutions in the areas of Commercial Vehicles, Construction Equipment, Tractor and Agriculture business. It services the priority sector by providing finance for Tractor, Crop loans, Small Enterprises and Allied agricultural activities, thereby helping the Bank meet its financial inclusion goal. In line with growing rural incomes, its Bank’s Commercial Bank branches have experienced robust growth across product lines on savings as well as lending side.

The Tractor Finance businesses reported significant growth and gained market share, while the Commercial Vehicle (CV) and Construction Equipment Business witnessed a sharp drop in disbursements due to excess load carrying norms, proposed change to BS-VI norms & a reduction in infrastructure spending by the Government. Asset quality also deteriorated.

The Bank’s Agriculture Financing business continued its focus on the agriculture value chain funding for various agro processing activities. It has registered good growth despite volatility and uncertainty in the commodities market. A Good monsoon and expectations of a bumper Rabi output supported the robust growth. Microfinance Institutions (MFI) segment growth remains robust and asset quality remains good.

Branches in semi-urban and rural areas come under the umbrella of the Commercial Bank. This network plays a crucial role in meeting the Bank’s financial inclusion goals and the credit demand of ‘Bharat’. The Commercial Bank’s Branch network has expanded and the Liabilities book has grown at a healthy pace.

Corporate Banking

The Bank’s Corporate Banking business caters to a wide range of corporate customer segments including major Indian corporates, conglomerates, financial institutions, public sector undertakings, multinational companies, small and medium enterprises and realty businesses. This business offers a comprehensive portfolio of products and services to these customers including working capital finance, medium term finance, trade finance, foreign exchange services, other transaction banking services, custody services, debt capital markets and treasury services. The core focus of this business has been to acquire deepen existing relationships and acquire new quality customers on a consistent basis, delivering customized solutions through efficient technology platforms backed by high quality service. The Bank also aims to secure value addition through the cross-selling of varied products and services.

Corporate Banking was subjected to a number of headwinds through the year including from a slowdown in the economy that was particularly visible in certain key segments such as auto & auto-ancillaries, telecom and real estate. The Bank has a higher proportion of working capital and short term assets and these were impacted due to the slowdown. The slowdown was compounded by elevated risks in the industry due to high leverage across sectors. In the face of this uncertainty, the Bank was cautious in increasing its exposures and concentration risks. The result has been a muted growth in Assets for the year.

Across corporate segments, the Bank has been proactive in rebalancing its portfolios to reflect economic situations and reducing exposure to situations with heightened risk. The Bank’s focus on risk management has helped the business reduce its Risk Weighted Assets (RWA) as a percentage of assets over the past few years. The use of Risk Adjusted Return on Capital (RaRoC) pricing models has become ingrained in the way the Corporate Banking division conducts its business and has helped to optimize pricing, better utilize capital and improve return on equity. Economic Value Add (EVA) measurement tools have been implemented that help the Bank monitor the true risk adjusted value being derived from each client. These initiatives ensure greater focus on improving income mix in favour of non-capital intensive income streams.

Improved credit spreads, higher non-credit income streams and controlled credit costs have ensured that the Bank has been able to grow the profitability of the Corporate Banking business at a strong rate and maintain a healthy Return on Equity (RoE).

The Bank continues on its Digital journey to provide the best in class solutions and enhance its customers’ experiences. During the year, Kotak Mahindra Bank has updated its Core Trade Platform which has laid the foundation for an integrated trade portal, have built a comprehensive Quickcheck platform to automate all types of recurring payments through error-free real time mandate registration, have built an Application Program Interface (API) based instant and end to end automated e-collections solution, have implemented the United Payments Interface (UPI) 2.0 recurring mandate solution and have partnered with FinTechs to provide API and Digital payment solutions. During this digital journey, the Bank has become the leading bank in Bharat Bill Payments System (BBPS), has built the Best in class Corporate Mobility Portal for providing on the go approvals and has been recognized as the Best Cash Management Bank by Asia Money and The Asian Banker. As part of its digital journey, Kotak Mahindra Bank is also upgrading its Cash Management Services (CMS) platform to enhance efficiency and experience, focusing on API based solutions and its use across its partners and customers and building a Loan Management and an Escrow Management solution to digitize the entire transaction process including the documentation process. Furthermore, Kotak Mahindra Bank has also provided Best in Class Structured solutions to various state and central governments, including its all in one and modular electronic fund flow application for National Health Mission, Rajasthan.

Wealth Management

Wealth Management, the Bank’s private banking arm, caters to a number of distinguished Indian families and is one of the oldest and the most respected Indian wealth management firms, managing wealth for 50% of India’s top 100 families (Source: Forbes India Rich List 2019), with customers range from entrepreneurs to business families and professionals.

The Bank provides an open architecture proposition to its customers, offering both proprietary and external wealth products. This business has a strong distribution capability for private clients through distribution/referral model across equities, fixed income & alternates across High Networth Individual (HNI) investors. In addition to comprehensive financial solutions, the family office service provides a strategic consolidated view on the client’s overall portfolio across multiple advisors, in addition to comprehensive financial solutions that go beyond investments. These include value added services such as assistance with investment structuring, banking and credit, consolidated reporting, referral for philanthropy services and concierge services. The trusteeship services offers estate planning services helping clients with succession planning activities through creation of private trusts. With an in-depth understanding of client requirements and expertise across various asset classes, this business offers the widest range of financial solutions through transaction-based investment approach. As per the Reserve Bank of India guidelines, advisory activities that were being offered out of the Bank are now offered out of Kotak Investment Advisors Limited, a subsidiary of the Bank with effect from 20th April, 2019.

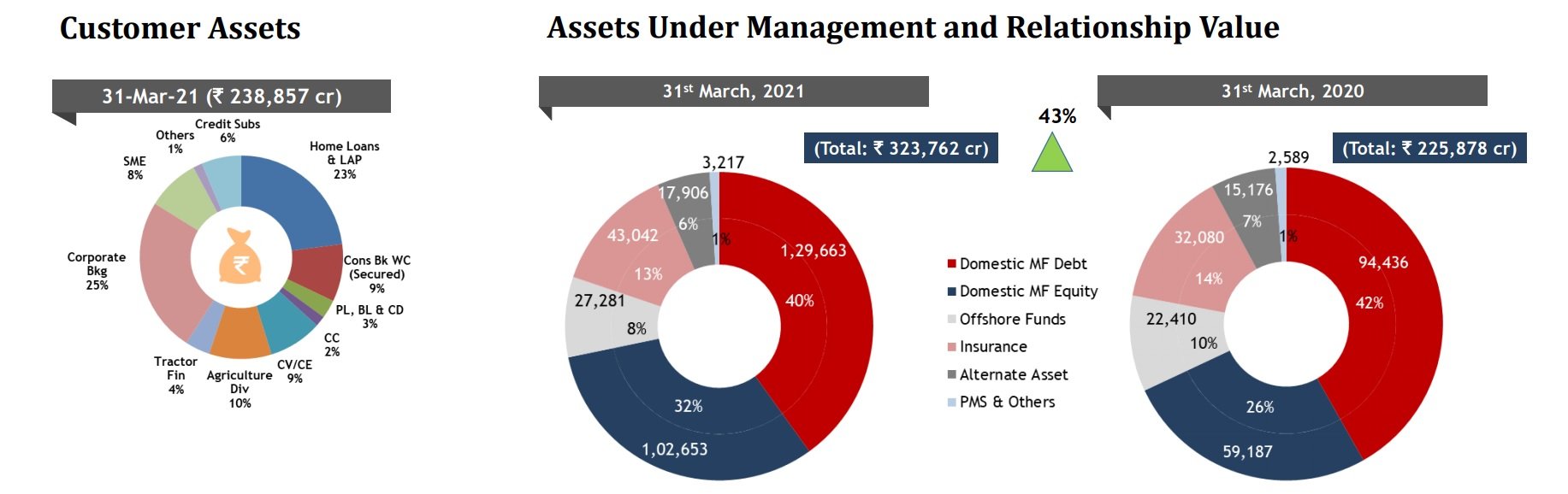

In addition, the Bank has also built a large Priority Banking business, assisting mass affluent customers with products and solutions developed to meet their financial requirements. The total relationship value across the Bank’s Wealth & Priority offerings is INR 306k crore (as of December 2019) across 4,400 families.

Asset Reconstruction

The Resolutions of several large accounts got seriously impacted due to slow down in the economy even before the Covid 19 crisis. It further exacerbated by the large unresolved piling of cases in various judicial forums like Debt Recovery Tribunals (DRT’s), Debt Recovery Appellate Tribunal (DRAT), High Courts, including National Company Law Tribunal (NCLT) proceedings under Insolvency and Bankruptcy Code (IBC).

The situation looks grim at the moment. The Reserve Bank of India has offered six months moratorium to all the standard borrowers which will give some breather to the borrowers to handle the financial crisis.

The company expect a lot of opportunities to present in the acquisition side, of the stressed loans which the Bank will look at very closely and if the prices offered are reasonable and attractive, the company shall be open to acquire several of them.

Financial Highlights

Kotak Mahindra Bank Q4 profit jumps 33% to Rs 1,682.4 crore 2

May 03, 2021; Kotak Mahindra Bank clocked a 32.8 percent year-on-year (YoY) growth in standalone profit at Rs 1,682.4 crore in the quarter ended March 2021, impacted by higher provisions. The profitability was supported by higher net interest income (NII), other income and pre-provision operating profit.

Numbers missed analysts' expectations. Profit was estimated at Rs 1,800 crore and NII at Rs 4,060 crore for the quarter, according to the average estimates of analysts polled by CNBC-TV18.

Net interest income in Q4 FY21 grew by 8 percent to Rs 3,842.81 crore compared to the year-ago, with moderate 1.8 percent YoY growth in advances at Rs 2.23 lakh crore during the quarter. However, net interest margin contracted to 4.39 percent from 4.72 percent in the same period.

Deposits, at Rs 2.8 lakh crore in the March quarter, grew by 6.6 percent year-on-year, missing analysts' expectations of over 10 percent growth.

Provisions and contingencies remained elevated at Rs 1,179.41 crore for the March quarter 2021, increasing 12.6 percent compared to the year-ago quarter and rose 181.8 percent QoQ.

During the quarter, the Supreme Court vacated the stay on NPA recognition and granted relief for interest on interest. Till December 2020, w.r.t cases not considered as NPA, Kotak Mahindra Bank had considered full hit for provisions and income as provisions for advances.

"Post the Supreme Court order, the bank has retrospectively, reversed income and consequently adjusted provisions and contingencies. Further, the bank has created a liability of Rs 110 crore towards estimated interest relief and has reduced the same from interest earned," said the bank.

The bank further said there was no fall in the COVID-19 provision during Q4 FY21. COVID-19 provisions were retained at Rs 1,279 crore as of March 2021, the bank added.

Total provisions (including specific, standard, COVID-19 related, etc.) as on March 2021 were Rs 7,021 crore, which was 95 percent of gross NPA, the bank said.

Non-interest income (other income) in Q4 FY21 surged 30.9 percent year-on-year to Rs 1,950 crore, while the pre-provision operating profit grew by 25 percent to Rs 3,407.5 crore compared to the year-ago quarter.

Asset quality weakened further in the March quarter with gross NPAs, as a percentage of gross advances, climbing to 3.25 percent compared to 2.26 percent in the previous quarter, while net NPA jumped to 1.21 percent at the end of Q4 FY21, compared to 0.5 percent in Q3 FY21. But gross and net NPAs dipped 2 bps and 3 bps respectively compared to proforma NPAs reported at the end of December 2020.

In the financial year FY21, the bank recorded a 17.1 percent growth in profit at Rs 6,965 crore and net interest income grew by 13.6 percent to Rs 15,340 crore compared to the previous year.

The consolidated profit of the bank stood at Rs 2,589 crore in Q4 FY21, up by 35.9 percent YoY. Subsidiary Kotak Mahindra Prime registered 14.3 percent YoY growth at Rs 184 crore, Kotak Securities' 47.9 percent growth at Rs 241 crore, and Kotak Mahindra Life Insurance' 17 percent growth at Rs 193 crore YoY. Among others, Kotak AMC and TC reported a 13.6 percent YoY growth in profit and international subsidiaries reported a 66.7 percent growth in profit during the quarter.

Recent developments

Kotak Mahindra Bank board approves proposal to raise Rs 5,000 crore via debt 3

May 29, 2021; Kotak Mahindra Bank on Saturday said its board has approved proposal to raise up to Rs 5,000 crore by issuing debt securities.

"The board of directors of Kotak Mahindra Bank, at its meeting held today i.e. on May 29, 2021 have, approved the proposal for issuance of unsecured, redeemable, non-convertible debentures/bonds/other debt securities, on private placement basis for an amount up to Rs 5,000 crore," the bank said in a regulatory filing.

The capital is to be raised in one or more tranches, subject to the approval of the members of the bank at the ensuing Annual General Meeting and any other approvals, it said.

References

- ^ https://www.kotak.com/content/dam/Kotak/investor-relation/Financial-Result/Annual-Reports/FY-2020/kotak-mahindra-bank/Kotak_Mahindra_Bank_Limited_FY20.pdf

- ^ https://www.moneycontrol.com/news/business/earnings/kotak-mahindra-bank-q4-profit-jumps-33-to-rs-1682-4-crore-provisions-remain-high-6848421.html

- ^ https://www.moneycontrol.com/news/business/markets/kotak-mahindra-bank-board-approves-proposal-to-raise-rs-5000-crore-via-debt-6960041.html