PNB Housing Finance Ltd

Summary

- PNB Housing Finance Limited is a registered housing finance company is promoted by Punjab National Bank (PNB).

- The Company operates through 94 branches and with over 21,000 channel partners to cover mass Indian market.

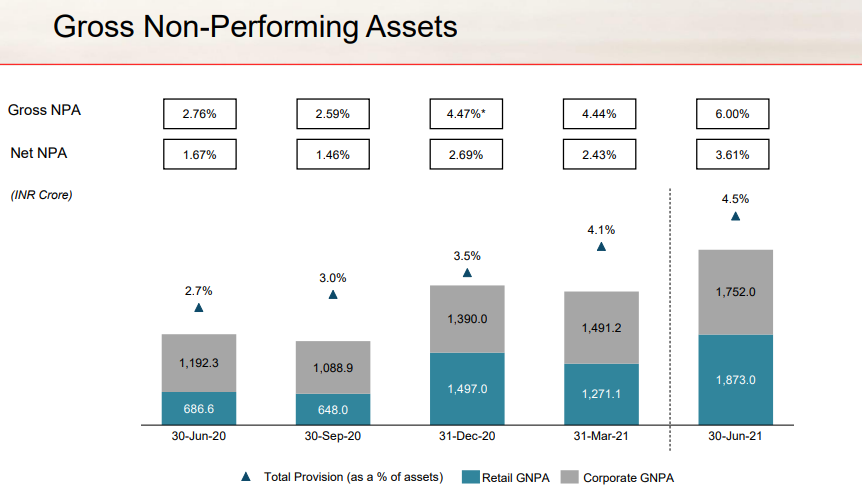

- NPAs spiked to 6 percent of the gross advances by June 30, 2021, from 2.76 percent a year ago.

Company Overview

PNB Housing Finance Limited (PNB Housing) (NSE:PNBHOUSING) is a registered housing finance company with National Housing Bank (NHB). It was incorporated under the Companies Act, 1956 and commenced its operations on November 11, 1988. PNB Housing is promoted by Punjab National Bank (PNB). The Company came out with a public issue of equity shares in November 2016. Its equity shares are listed on National Stock Exchange (NSE) and Bombay Stock Exchange (BSE) with effect from 7th November 2016. 1

With over three decades of specialised experience in housing finance, PNB Housing has a robust network of branches spread across the country which help its customers avail financial services (loans and deposits) seamlessly.

PNB Housing provides housing loans to individuals and corporate bodies for purchase, construction, repair and upgradation of houses. It also provides loans for commercial space, loan against property and loan for purchase of residential plots.

As on March 31, 2021, the Company has presence through 94 branches, 17 outreach locations, totalling to 111 distribution outlets. The Company also has 22 underwriting hubs for credit decision making.

Products and Offerings

Home Loan

- Home Purchase Loan

- Home Construction Loan

- Home Extension Loan

- Home Improvement Loan

- Residential Plot Loan

- Loan For Nris

- Unnati Home Loans

- Pradhan Mantri Awas Yojana

Non Home Loans

- Commercial Property Loan

- Loan Against Property

- Lease Rental Discounting

- Loan For Real Estate Developers

Fixed Deposit

Industry Overview

The HFCs were already seeing a muted demand environment in FY 2019-20. The COVID-19 pandemic further aggravated the situation. This resulted in a slowdown in disbursements in FY 2020-21, and the cumulative growth in on-book portfolio of HFCs for 9M FY 2020-21 (December 2020 vs. March 2020) stood at 2%. However, the second half of the year witnessed recovery in demand, leading to a gradual increase in disbursements, nearing pre-COVID levels. As per ICRA, total housing credit increased from Rs 21.1 lakh crores as on March 31, 2020 to Rs 22.1 lakh crores as on December 31, 2020. The affordable housing segment remains one of the key demand drivers and the Government of India extending the credit-linked subsidy scheme (CLSS) to March 2021 provided fillip to the sector. In the Budget 2021, the government has further extended the CLSS scheme till March 2022, driving demand in the affordable housing sector.2

Given the COVID-19 induced disruptions, the industry saw moderation in the growth rate and the overall on-book housing portfolio reported nil growth (Q-o-Q) in Q1 FY 2021. The disbursements started picking up from Q2 FY 2021 onwards and the overall on-book housing loan portfolio of NBFCs/HFCs and banks is estimated to have reached Rs 22.1 trillions as on December 31, 2020. Supported by portfolio buyout, banks continued to outpace the disbursement growth. The overall HFC credit in India is estimated at Rs 11.3 lakh crores as on December 31, 2020, with exposures across home loans (HL), loan against property (LAP), construction finance (CF), and lease rental discounting (LRD).

Driven by robust demand and liquidity support from the National Housing Bank, the portfolio growth in the affordable segment remained higher at 8% in 9M FY 2021, following the growth of 18% in FY 2019-20. With unwavering demand, the segment is expected to continue growing at a faster pace than the overall industry

Asset Quality Remains a Worry

The overall gross non-performing assets (NPA) (stage 3 assets as per revised Ind-AS June 2018 onwards) increased to 2.4% as on March 31, 2020 (1.6% as on March 31, 2019) due to a deterioration across HFCs in the construction finance and LAP segments. The asset quality witnessed further deterioration, although the same is not reflected in the reported numbers as on December 31, 2020. This was largely owing to the asset classification dispensation as per the order by the Hon’ble Supreme Court for not classifying accounts as NPAs till a further order is announced. However, this was settled in March 2021 as the apex court passed an order to lift blanket ban on classification of non-performing assets (NPAs).

Nevertheless, as witnessed in the delinquencies/stage-3 assets reported by entities, the asset quality has witnessed deterioration in Q3 FY 2021 and a further impact is expected in Q4 FY 2021. The proforma NPAs (those considering no asset classification dispensation) increased to around 2.7% (around 60 basis points higher than reported numbers as on December 31, 2020). Some entities have resorted to the restructuring option available under the regulatory relief measures announced by the RBI.

Skewed Borrowing Profile

Owing to the challenges in the last two years, the HFCs have reduced funding from CPs and its share has declined to around 2% as on December 31, 2020, from 4% as on March 31, 2020 (7% as on March 31, 2019). The proportion of fixed deposits increased considerably to 21% as on December 31, 2020, from 16% as on March 31, 2020.

The borrowing profile of HFCs remains skewed towards the NCDs, comprising around 38% of the total debt (including off-book). The HFCs witnessed a 9% y-o-y increase in bond issuances in 9M FY 2021 compared to an 18% y-o-y decline in FY 2019-20. Though the funding requirement has been relatively low, given the slowdown in disbursements, the entities are expected to have refinanced a part of their existing high-cost debt as the fresh issuances took place at lower yields. Moreover, the issuances continued to be dominated by the top few issuer, with the top five issuers among HFCs accounting for more than 80% of the bond issuances in 9M FY 2021.

Adequate Capitalisation but High Provisioning

The aggregate on-balance sheet gearing of HFCs stood at 4.8x as on December 31, 2020 as against 5.4x as on March 31, 2020. Despite the high leverage of many HFCs, the reported capital adequacy remained good with a median CRAR of 18.3% as on December 31, 2020, supported by the relatively lower risk weights for home loans and Corporate loans for residential projects.

Outlook for the Sector

The housing finance sector is positioned attractively in the coming years driven by strong demand, especially in the affordable housing sector. This is further reinforced by the fact that a number of A-rated builders in the country are moving towards affordable housing segment driven by the Tax SOPs offered by the government. On the other hand, the extension of the CLSS scheme by the Government of India for the affordable housing segment is expected to drive growth within the sector. Additionally, following the pandemic, there has been an increasing trend of owning homes, which is also aiding in driving the housing finance sector in the country. Mortgage penetration in India continues to be lowest when compared with the developed countries, which indicates strong growth opportunity for the sector in the coming years.

Business Overview

During the year, the company focused on strengthening its balance sheet and placed greater emphasis on diversification into areas where the company want to build a stronghold. The company undertook several steps to increase its presence in the retail segment. The company also focused on deleveraging and reducing the load of asset on its capital, which in turn, would reduce the gearing. PNB Housing Finance was able to achieve this by placing greater focus on building granular book, strategic shift towards a retail-focused segment and reduction in the corporate book share via sell down/accelerated pre-payments. The measures resulted in improvement of its capital adequacy ratio from 14% as on March 31, 2019 to 18.7% as on March 31, 2021.

Lending Operations

In terms of business, retail segment accounted for 96% of disbursements, as compared to 92% the year before, resulting in retail segment to be 84% of its assets under management (AUM) as on March 31, 2021. The company optimised its branch network through merging branches and shifting them to a low-cost setting in Tier 2 and Tier 3 cities, thereby enabling it to increase its disbursements from these cities. The retail disbursements from Tier 2 and Tier 3 branches increased to 42% in FY 2019-20 as compared to 40.7% in FY 2019-20 resulting in increased share of retail assets under management (AUM) from Tier 2 and Tier 3 branches to around 37% as on March 31, 2021 from around 34% as on March 31, 2020. With focus on building granular book, the disbursements in less than Rs 2 crores ticket size reduced to 7% of the retail disbursements in FY 2020-21 from 13% in FY 2019-20. The company also tightened its lending norms and implemented a robust IT framework across the organisation, which optimised its operations significantly.

The company sanctioned 50,454 loan applications during FY 2020-21. The disbursements for FY 2020-21 stood at Rs 10,445 crores compared to Rs 18,626 crores for FY 2019-20. Assets under management (AUM) was at Rs 74,469 crores as on March 31, 2021.

Individual Housing Loans

Owing to its increased focus on the retail segment and growing pie of the affordable housing segment, its average ticket size of the loan stood at Rs 27 lakhs as on March 31, 2021 against Rs 29 lakhs as on March 31, 2020 for Individual Housing Loan. Salaried customers accounted for 70% of the individual housing loans, while self-employed customers contributed 30%. The company's conservative approach towards underwriting and disbursement led to the Loan-to-Value (LTV) for individual housing loan at 72% as on March 31, 2021. The company continued its focus on financing ready properties, resulting in the share of the under-construction portfolio in the individual housing AUM declining from 19% as on March 31, 2020, to 17% as on March 31, 2021.

The Company in its efforts to support the Government scheme of “Housing for All” through PMAY-CLSS scheme, have cumulatively disbursed ~ Rs 12,000 crores under ~56,000 loan accounts in the category of EWS/LIG and MIG I/MIG II upto March 31, 2021.

Unnati Loans

There has been a growing focus on the Unnati segment, which led to increase in book during the year. Unnati Book stands at Rs 2,985 crores with average ticket size of Rs 18 lakhs. Salaried segment contributed 58% of the loans and balance 42% by self employed segment.

Retail Loan Against Property

During the year, the Company disbursed Rs 2,526 crores under this segment. The Average Ticket Size (ATS) is at Rs 44 lakhs as on March 31, 2021 compared to Rs 47 lakhs as on March 31, 2020.

The weighted average LTV was maintained below 50%. The self-employed segment accounts for 80% of the retail LAP book. Over time with focus on the lower ticket size, the Loan Asset of LAP book in more than Rs 2 crores has reduced by over 4% during the year to 33.6% as on March 31, 2021 from 37.7% as on March 2020.

Construction Finance Loan

Construction finance book comprised 12% of the AUM as on March 31, 2021. The ATS on a unique corporate house basis is Rs 167 crores. The construction finance book is spread across 79 unique developers, with top seven markets contributing 89% of the AUM. As per laid out strategy to reduce corporate book, the construction finance book in last one year reduced by 17% in absolute terms to Rs 8,637 crores as on March 31, 2021 from Rs 10,356 crores as on March 31, 2020.

Corporate Term Loan

Corporate term loan (loans given to the developers either for construction of commercial units or as a term loan secured against a mortgage) comprised 3% of the AUM, as on March 31, 2021. The ATS on a unique corporate house basis is Rs 98 crores. The corporate term loan book is spread across 40 unique developers, with top seven markets contributing to 90% of the AUM. The corporate term loan book in last one year reduced by 27% in absolute terms to Rs 2,243 crores as on March 31, 2021 from Rs 3,052 crores as on March 31, 2020.

Lease Rental Discounting

It includes the loans given to the developers against the rental receipts derived from lease contracts with corporate tenants. The share of this book in the total AUM stood at 1% as on March 31, 2021 and the ATS on a unique corporate house basis is Rs 84 crores. The LRD book is spread across 11 unique developers, with a presence in seven large cities. 100% of the LRD book is backed by leased out commercial office buildings with multiple tenants. The lease rental discounting loan book in last one year reduced by 25% in absolute terms to Rs 906 crores as on March 31, 2021 from Rs 1,206 crores as on March 31, 2020.

PHFL Home Loans and Services Limited (PHFL)

The company's wholly-owned subsidiary, PHFL is focused on sales and distribution functions of PNB Housing Finance. It has helped in reducing dependence on external sources for acquiring new businesses. PNB Housing Finance has also been providing adequate processing support to ease the delivery process for customers.

Expected Credit Loss Provisions

As on March 31, 2021, being prudent considering the external challenges of higher delinquencies on account of COVID-19 disruption and degrowth in the overall portfolio, the company made provisions of Rs 778 crores during the year resulting in total provision of Rs 2,544 crores as on March 31, 2021. The company's total provision to total assets stood at 4.1%, increased from 2.6% as on March 31, 2020. The provision coverage ratio for Stage 3 moved up to 45.2% as on March 31, 2021 from 36.2% as on March 31, 2020.

Financial Highlights

During the year ended 31 March 2021, the Company has earned a total income of Rs 7,624.08 crores as compared to Rs 8,489.55 crores in the previous year, recording a decline of 10.19%. Total expenses, provisions and write offs during the year were Rs 6,417.05 crores as compared to Rs 7,678.54 crores in the previous year, a decline of 16.43%.

During the year, the Company has earned Pre-provision Operating Profit of Rs 2,068.93 crores as compared to Rs 2,062.38 crores in the previous year.

During the year, the Company has earned a Profit before Tax of Rs 1,207.03 crores as compared to Rs 811.01 crores in the previous year, recording an increase of 48.83%. The Profit after Tax during the year was Rs 929.90 crores as compared to Rs 646.24 crores in the previous year, an increase of 43.89%.

As per IND AS, during the year, the Company has made Expected Credit Loss (ECL) provision (on loan assets) of Rs 778.50 crores as compared to Rs 1,171.49 crores in the previous year. The Company is carrying total ECL provision of Rs 2,544.11 crores.

The Capital Adequacy Ratio (CRAR) as on March 31, 2021, was 18.73% (comprising Tier I capital of 15.53% and Tier II capital of 3.30%). The Reserve Bank of India (RBI) has prescribed minimum CRAR of 14% of total risk weighted assets for FY 21

The Company has sanctioned loans amounting to Rs 15,301 crores in respect of 50,454 loan applications, as compared to Rs 24,503 crores in respect to 73,553 loan applications in the previous year, decline of 31% in number of loan applications received and decline of 38% in loan sanctioned amount.

During the year, the Company has disbursed loans amounting to Rs 10,445 crores as compared to Rs 18,626 crores in the previous year, decline of 44%. With retail focussed lending, during FY 21, 96% of loans disbursed were in retail segment.

During the year, the Company disbursed subsidy under PMAY scheme in 12,412 accounts with a sanction value of Rs 2,809 crores. The total subsidy transferred in the beneficiary accounts amounted to Rs 297 crores.

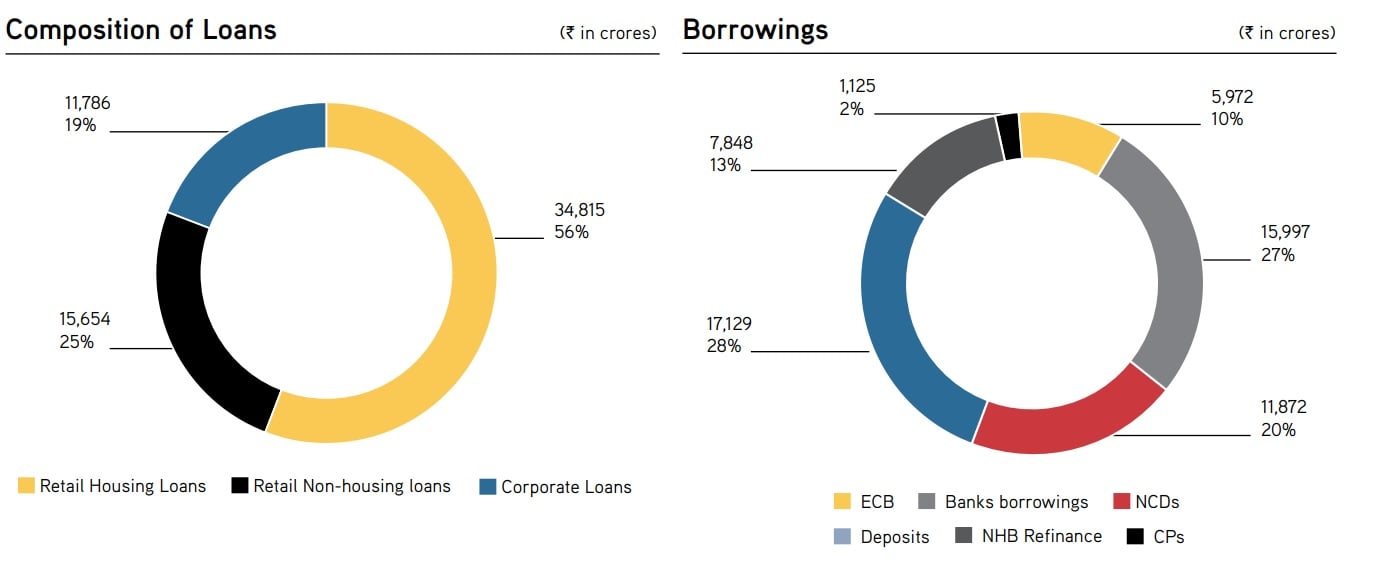

Loan Book

Principal outstanding of loans as at March 31, 2021 were Rs 62,255 crores. The Assets Under Management (AUM) as at March 31, 2021 were Rs 74,469 crores. Further details of lending operations are provided in the MD&A.

Borrowings

During the year, the Company has raised fresh resources of Rs 29,131 crores from multiple sources. The Company also securitised Rs 789 crores in FY 21 through direct assignment route. The Company repaid short and long-term borrowings of Rs 37,405 crores.

Deposits

The Company has raised Rs 7,289 crores of fresh deposits during the year. The outstanding deposits (including inter corporate deposits) as at March 31, 2021, were Rs 17,129 crores as against Rs 16,470 crores (including inter corporate deposits) outstanding last year, registering a growth of 4%.

June 30, 2021 Result

August 05, 2021; PNB Housing Finance its consolidated net profit fell over 5 percent to Rs 243.28 crore for the first quarter ended June 30, as the business was impacted due to the second wave of the coronavirus pandemic.3

The non-banking finance company had posted a net profit of Rs 257.18 crore in the year-ago period. On a sequential basis, it was higher than Rs 127 crore in the March 2021 quarter.

On its proposed Rs 4,000 crore capital raise plan, PNB Housing Finance said: "The company on 20th June 2021, filed an appeal before the Securities Appellate Tribunal (SAT) against the letter issued by SEBI. The case is currently sub-judice under SAT with the final order awaited".

The deal was announced on May 31, 2021, in which a clutch of investors led by a US-based Carlyle group will pick up equity and warrants of the company for a Rs 4,000 crore fund infusion.

Under the deal, Pluto Investments S.a.r.l. and Salisbury Investments Pvt Ltd would acquire an equity stake in PNB Housing Finance. State-owned Punjab National Bank holds a little over 32 percent stake in the company.

The issue, which is subject to legal, shareholder and regulatory approvals, has reached the SAT after it came under the lens of markets regulator Sebi for valuation of the shares to be offered.

PNB Housing Finance has challenged Sebi's directive and the matter is before the Securities Appellate Tribunal (SAT), which has reserved its order.

Meanwhile, in a significant development, the Competition Commission has given its nod for the proposed investments by Carlyle Group and other investors in PNB Housing Finance Ltd.

The transaction has been approved by the Competition Commission of India (CCI) under the Green Channel.

The equity and warrants are fixed to be issued at Rs 390 a share, much lower than the current prevailing price of the company's shares on the stock exchanges.

The total income (consolidated) of PNB Housing fell to Rs 1,692.88 crore in Q1FY22, as against Rs 1,872.33 crore in Q1FY21, the company said in a regulatory filing.

On a standalone basis, the net profit during the quarter was Rs 234.96 crore, compared to Rs 259.61 crore a year ago.

The total income stood at Rs 1,676.45 crore in June 2021 quarter, lower than Rs 1,868.58 crore in the year-ago period.

"The second wave of COVID-19 impacted the business performance of the company as compared to last quarter. Despite this, the company recorded healthy profits and margins during the quarter. The company continues to focus on increasing its digital footprints, grow retail business with efficient underwriting and collection models and optimise costs to create value for all its stakeholders," Hardayal Prasad, Managing Director and CEO, PNB Housing Finance, said.

The net interest income grew nearly 13 percent to Rs 550 crore during the quarter from Rs 448 crore in the year-ago period.

On the asset front, the gross non-performing assets (NPAs or bad loans) spiked to 6 percent of the gross advances by June 30, 2021, from 2.76 percent a year ago.

The net NPAs too soared to 3.61 percent from 1.67 percent.

The company's gross NPAs stood at Rs 3,625 crore by end of Q1FY22. It also made provisions worth Rs 2,700 crore against expected credit loss (ECL). It held Rs 995 crore as a regulatory provision, following the National Housing Bank (NHB) norms.

The CRAR (capital to risk-weighted assets ratio) improved to 21.4 percent by June-end this year from 18.73 percent.

However, the cost to income ratio rose to 16.6 percent from 15.1 percent, mainly because of lower fee income to lesser disbursements as business operations were impacted due to the lockdown.

PNB Housing said it will continue to focus on its affordable housing "Unnati" book, which registered a growth of 163 percent year-on-year in disbursements during the quarter at Rs 123 crore.

The loan book under Unnati stands at Rs 2,986 crore.

The total disbursements during the quarter stood at Rs 1,759 crore. Of this, Rs 1,652 crore was towards retail and Rs 107 crore towards corporate.

Prasad said the company continues to reduce its corporate book and focuses on the retail segment.

On its corporate book remedial actions, the company said it has achieved resolutions in IREO Pvt Ltd with an outstanding of Rs 150 crore with zero haircuts; Windlass Developers Rs 30 crore; Pate Developers Rs 20 crore (nil haircut) and three other NPA accounts with Rs 4 crore outstanding and nil credit loss.

Besides, the accounts of Vipul Ltd (Rs 353 crore outstanding) and Ornate Pvt Ltd (Rs 181 crore) are in the final stages of resolution.

Resolutions are underway on NPA accounts -- Supertech Ltd (Rs 244 crore); Radius (Rs 259 crore) and Arena Superstructure Pvt Ltd (Rs 187 crore).