Square

Business

Square (SQ) started Square in February 2009 to enable businesses (sellers) to accept card payments, an important capability that was previously inaccessible to many businesses. However, sellers also need innovative solutions to thrive, and Square has since expanded to provide additional products and services to give these businesses access to the same tools as large businesses. This approach aligns with its purpose of economic empowerment, as everything the company do should give sellers accessible, affordable tools to grow their businesses and participate in the economy.1

Square is a cohesive commerce ecosystem that helps its sellers start, run, and grow their businesses. The company combine sophisticated software with affordable hardware to enable sellers to turn mobile and computing devices into powerful payment and point-of-sale solutions. Square has high seller acceptance rates and fast onboarding, while maintaining low risk and fraud losses as a result of its approach to risk management that emphasizes data science and machine learning. The company focus on technology and design to create products and services that are cohesive, fast, self-serve, and dependable. These attributes differentiate it in a fragmented industry that forces sellers to stitch together hardware, software, and payments services from multiple vendors.

The foundation of its ecosystem is a full service, managed payments offering. Once a seller downloads the Square Point of Sale mobile app, they can quickly and easily take their first payment, because the company can typically bring them onto its system in minutes. With its offering, a seller can accept payments in person via magnetic stripe (a swipe), EMV (Europay, MasterCard, and Visa) (a dip), or NFC (Near Field Communication) (a tap); or online via Square Invoices, Square Virtual Terminal, or the seller’s website or app. Once on its system, sellers gain access to technology and features such as reporting and analytics, next-day settlements, digital receipts, payment dispute and chargeback management, security, and Payment Card Industry (PCI) compliance. In the same way that Square has empowered businesses with fast, simple, and cohesive tools, the company see an opportunity with Cash App to build a similar ecosystem of services for individuals. Currently, its Cash App offers individuals access to a fast, easy way to send and receive money electronically to and from individuals and businesses. The company also offer Cash App customers the ability to use their funds via a Visa debit card. Square has also recently added functionality to Cash App to enable customers to buy and sell bitcoin.

The company's commerce ecosystem also includes powerful point-of-sale software and services that help sellers make informed business decisions through the use of analytics and reporting. As a result, sellers can manage orders, inventory, locations, employees, and payroll; engage customers and grow their sales ; and gain access to business loans through its Square Capital service. The company monetize these features through either a per transaction fee, a subscription fee, or a service fee. Some of these advanced point-of-sale features are broadly applicable to its seller base and include Employee Management and Customer Engagement. Square has also extended its ecosystem to serve sellers with more specific needs. The company's Build with Square developer platform (application programming interface or APIs) allows businesses with individualized needs to customize their business solutions, including integration with third-party applications, while processing payments on Square and taking advantage of all the services in its ecosystem. In addition, certain verticals, such as services and retail sellers, benefit from specific features such as Invoices, Appointments, and Square for Retail. The company also serve sellers through Caviar, a food ordering service for pickup and delivery that helps restaurants reach new customers and increase sales without additional overhead.

Square has grown rapidly to serve millions of sellers that represent a diverse set of industries, including retail, services, and food-related businesses, and sizes, ranging from a single vendor at a farmers’ market to multi-location businesses. These sellers also span geographies including the United States, Canada, Japan, Australia, and the United Kingdom. The company believe the diversity of its sellers underscores the accessibility and flexibility of its offerings. In the year ended December 31, 2017, the company processed $65.3 billion of Gross Payment Volume (GPV), which was generated by 1.4 billion card payments from approximately 287 million payment cards. The company processed $49.7 billion and $35.6 billion of GPV in 2016 and 2015, respectively.

The company's ability to add new sellers efficiently, and help them grow their business after they join its platform, has led to continued and sustained growth. The company's existing sellers also represent a sizable opportunity to up-sell and cross-sell products and services with little incremental sales and marketing expense.

Products and Services

Managed Payments Solutions

The foundation of its ecosystem is a full service, managed payments offering. Sellers can onboard to Square in minutes and, once onboarded, accept payments in person via swipe, dip, or tap of a card; online via Square Virtual Terminal or the seller’s website or app; or through the Cash App. By paying a transparent transaction fee, sellers receive technology and features that allow them to manage the entire payment lifecycle, including reporting and analytics, next-day settlements (or instant settlement for an additional transaction fee via Instant Deposit), digital receipts, payment dispute and chargeback management, security, and PCI compliance. Transaction-based revenue as a percentage of GPV was 2.94%, 2.93%, and 2.95% in the years ended December 31, 2017, 2016, and 2015, respectively.

Hardware

The company's affordable, custom-designed hardware can process all card payment forms, including magnetic stripe, EMV chip, and NFC technology. Sellers can accept Visa, MasterCard, American Express, or Discover for one transaction fee. Additionally, sellers in Canada can accept Interac Flash, and sellers in Japan can accept JCB. The company's hardware includes the following products:

- Magstripe reader: The company's magstripe reader enables swiped transactions of magnetic stripe cards by connecting with an iOS or Android smartphone or tablet.

- Contactless and chip reader: This reader accepts EMV chip cards and NFC payments, enabling acceptance via Apple Pay, Android Pay, and other mobile wallets. The reader connects wirelessly or via USB.

- Chip card reader: The company's chip card reader accepts EMV chip cards and enables swiped transactions of magnetic stripe cards by connecting with an iOS or Android smartphone or tablet.

- Square Stand: This hardware enables an iPad to be used as a payment terminal or full point of sale solution. It features an integrated magnetic stripe reader, provides power to a connected iPad, and can connect to the contactless and chip reader wirelessly or via USB. Square Stand also connects to various peripheral devices that brick-and-mortar businesses need, such as barcode scanners and receipt printers.

- Square Register: During the fourth quarter of 2017, the company launched Square Register, its first all-in-one offering that combines its hardware, point-of-sale software, and payments technology. Square Register does not require a third- party mobile phone or tablet, and it contains connections for Ethernet, Wi-Fi, and a USB hub so sellers can integrate with peripheral devices. The dedicated hardware consists of two screens: a seller display and a customer display with a built-in card reader that accepts tap, dip, and swipe payments.

Software

Square Point of Sale is its point-of-sale software that can be downloaded to an iOS or Android device, is pre-installed on Square Register, and is designed to get a seller (and their employees) up and running quickly. It consists of managed payments solutions and advanced software products, all of which are integrated with one another to provide both sellers and their buyers with a cohesive experience that is fast, self-serve, and dependable. Square Point of Sale includes Square Dashboard, its cloud-based reporting and analytics tool that provides sellers with real-time data and insights about sales, items, customers, and employees. This enables sellers to make informed decisions about their business.

Within Square Point of Sale or Square Dashboard, a seller can use Square Invoices to securely collect payments by creating a custom digital invoice and then sending it to their customer. Square Invoices is integrated with Customer Directory and synced across Square Point of Sale and Square Dashboard, allowing the seller to easily track invoices, send payment reminders to the customer, and set recurring billing. Sellers may use Square Invoices for upcoming or previously-delivered goods and services, such as catering orders, contractor services, and retail orders. Sellers pay only a transparent transaction fee for this managed payments solution.

For sellers with a more complex business or multiple employees and/or locations, the company offer additional advanced functionality. Location and employee management allows a seller to track sales by location, device, or employee; customize employee permissions; and create employee timecards. Square Payroll empowers sellers to grow by making it easy to hire, onboard, and pay wages and associated taxes for employees. Square Customer Directory, Feedback, Loyalty, and Marketing provide CRM (customer relationship management) tools that help sellers engage their buyers to grow their business. By linking customer data with point-of-sale and transaction data, the company can offer its sellers targeted marketing campaigns and a closed-loop system that allows sellers to easily assess the return on investment of their marketing efforts. The company monetize all these features through either a per transaction fee, a subscription fee, or a service fee.

Additionally, the company continue to build vertical solutions to better meet the needs of specific industries, such as services, retail, and food-related sellers. With its Square Appointments app, sellers in the services industry have one integrated solution from which they can create a seamless experience from booking to payment. Customers can easily schedule appointments with their preferred time, service, and staff member, and sellers can send invoices to their customer’s email address. With Square for Retail, sellers in the retail industry have an end-to-end point-of-sale solution with sophisticated inventory management that fully integrates with its managed payments and hardware. It has a search-based user interface and fast barcode scanning; advanced inventory management that supports tens of thousands of items, cost of goods sold, purchase orders, vendor management; and employee management capabilities that allow retail sellers to better understand their customers’ habits.

Open Developer Platform

Square has opened Square to reach sellers who want access to its ecosystem but also want flexibility in their solutions to meet their individualized business needs. Build with Square is its developer platform, consisting of APIs that allow sellers and their developers to customize business solutions. The company's Point-of-Sale API allows sellers to integrate any iOS or Android point of sale with Square to accept payments and access all other services in the ecosystem. This is particularly useful for sellers with highly-individualized point-of-sale needs. With its e-commerce API, sellers can integrate Square with their e-commerce website or app.

As the company continue to expand Build with Square, sellers tell it they want to connect Square to more of their business systems. Square has APIs for sellers to manage their item catalog more effectively, such as implementing real-time price changes at scale (e.g., for holiday promotions), and to connect their inventory to their online sales. This generates integrated reporting across sales channels, which is especially important for businesses that sell online and in person and share inventory between channels. Build with Square also has APIs for sellers to integrate Square with other business solutions such as accounting, CRM software, customer databases, employee management and ERP software. And through the Square App Marketplace, sellers can integrate Square with third-party apps, such as QuickBooks or BigCommerce, that create extensions to its point-of-sale functionality and other back office solutions, and enables sellers to integrate all of their business data.

Cash App

Cash App is empowering individuals by providing access to the financial system, allowing customers to electronically send, store, and spend money. Individuals and businesses can sign up for a Cash App account simply using a debit card, bank account, or credit card and an email address or a phone number. Businesses can use Cash App to accept payments from their customers (Cash for Business). Cash App originally enabled customers to send and track P2P (peer-to-peer) payments and deposit stored funds into their bank account. Square has added features to provide individuals with more ways to add and spend stored funds. Customers can receive direct deposit payments (such as those from an employer) or ACH payments from a financial institution. And customers can use their Cash Card, a Visa debit card, to make purchases or to withdraw funds at ATMs (automated teller machines). Square receives a fee when customers elect to have their funds instantly deposited to their bank accounts and for transactions conducted with Cash Card or a credit card. Additionally, in the fourth quarter of 2017, the company added functionality to the Cash App that enables individuals to use their stored funds to buy bitcoin. Customers can also sell their bitcoin to it. As of December 31, 2017, the value of bitcoin transactions was immaterial as was the impact of bitcoin transactions on its consolidated financial statements. In the same way that Square has provided businesses with fast, simple, and cohesive tools, the company see an opportunity with Cash App to build a similar ecosystem of services for individuals.

Caviar

Caviar is its food ordering platform, which is another service the company offer that helps sellers grow and provides a differentiated way to service restaurants, a large target market for managed payments and point-of-sale solutions. This service makes it easy for restaurants to offer food ordering, both pickup and delivery, to their customers, enabling them to expand their sales and grow revenue without additional overhead. Individuals can order food from local restaurants through the Caviar website or mobile app, which is purpose-built to make delivery and pickup fast and easy. Caviar is currently available in many U.S. markets, including but not limited to New York, San Francisco, and Philadelphia, with thousands of partner restaurants. Caviar charges consumers a delivery and service fee per order. The company also charge its partner restaurants a seller fee as a percentage of total food order value.

Square Capital

Square Capital, through a partnership with an industrial bank, facilitates the offering of loans to pre-qualified sellers based on real-time payment and point-of-sale data. These customized loan offers eliminate the lengthy (and often unsuccessful) loan application process for the seller, while facilitating prudent risk management. The terms are straightforward for sellers, and once approved, they get their funds quickly, often the next business day. Sellers can use these funds to make investments in their business, such as purchasing inventory or equipment, hiring additional employees, expanding their stores, or opening new locations.

Generally, loan repayment occurs automatically through a fixed percentage of every card transaction a seller takes. By simply running their business, sellers repay their loan within an average of nine months. The company currently fund a majority of these loans from arrangements with institutional third-party investors who purchase these loans on a forward-flow basis. This funding significantly increases the speed with which the company can scale Square Capital services and allows it to mitigate its balance sheet and liquidity risk.

Since its public launch in May 2014, Square Capital has facilitated over 400,000 loans and advances, representing $2.5 billion.

Sellers

The company's sellers represent a diverse range of industries, including retail, services, and food-related businesses. The company serve sellers of various sizes, ranging from a single vendor at a farmers’ market to multi-location businesses. These sellers also span geographies including the United States, Canada, Japan, Australia, and the United Kingdom. The company believe the diversity of its sellers underscores the accessibility and flexibility of its offerings.

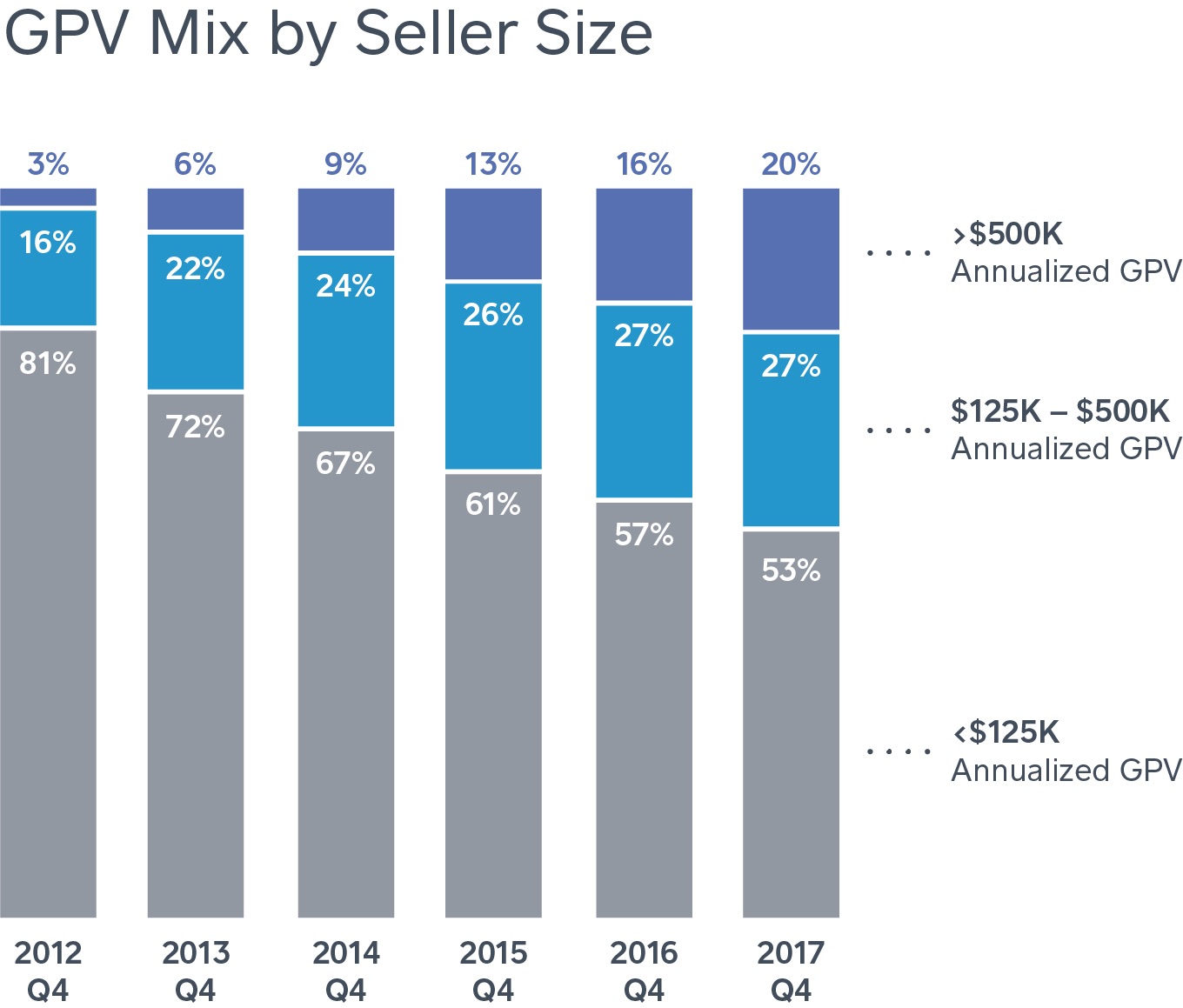

Square is increasingly serving larger sellers, which the company define as sellers that generate more than $125,000 in annualized GPV. GPV from larger sellers represented 48% of total GPV in the fourth quarter of 2017, up from 43% in the fourth quarter of 2016 and 39% in the fourth quarter of 2015. For the years ended December 31, 2017 and 2016, the company had no customer who accounted for greater than 10% of its GPV or its total net revenue. For the year ended December 31, 2015, the company had no customer other than Starbucks who accounted for greater than 10% of its GPV or its total net revenue.

The chart below shows the mix of its GPV by seller size:

Sales and Marketing

Square has a strong brand and continue to increase awareness of Square among sellers by enhancing its services and fostering rapid adoption through brand affinity, direct marketing, public relations, and strategic partnerships. The company's Net Promoter Score (NPS) has averaged nearly 70 over the past four quarters, which is double the average score for banking providers. The company's high NPS means its sellers recommend its services to others, strengthening its brand and helping to drive efficient customer acquisition.

Direct marketing, online and offline, has also been an effective customer acquisition channel. This includes online search engine optimization and marketing, online display advertising, direct mail campaigns, direct response television advertising, mobile advertising, affiliate and seller referral programs. Total advertising costs for the years ended December 31, 2017, 2016, and 2015 were $81.9 million, $58.3 million, and $58.3 million, respectively. Additionally, Square hardware products, such as its contactless and chip reader or Square Stand, are available at over 30,000 retail stores (including Apple, Amazon, Best Buy, Staples, Target, and Walmart). The company's direct sales and account management teams also contribute to the acquisition and support of larger sellers. In addition to direct channels, the company work with third-party partners and developers who offer its solutions to their customers.

The company's direct, ongoing interactions with its sellers help it tailor offerings to them, at scale, and in the context of their usage. The company use various scalable communication channels, such as email marketing, in-app notifications and messaging, dashboard alerts, and Square Communities, its online forum for sellers, to increase the awareness and usage of its products and services with little incremental sales and marketing expense.

Product Development and Technology

The company design its products and services to be cohesive, fast, self-serve, and dependable, and the company organize its product teams accordingly, combining individuals from product management, development and engineering, data science, and design.

The company's products and services are mobile-first and platform-agnostic, and Square is able to continuously optimize them because its hardware, software, and payments processing are integrated. The company frequently update its software products and have a regular software release schedule with improvements deployed generally twice a month, ensuring its sellers get immediate access to the latest features. The company's services are built on a scalable technology platform, and the company place a strong emphasis on data analytics and machine learning to maximize the efficacy, efficiency, and scalability of its services. This enables it to capture and analyze over a billion transactions per year and automate risk assessment for more than 99.95% of all transactions. The company's hardware is designed and developed in-house, and the company contract with third-party manufacturers for production. The company's product development expenses were $321.9 million, $268.5 million and $199.6 million for the years ended December 31, 2017, 2016, and 2015, respectively.

Transaction Processing Overview

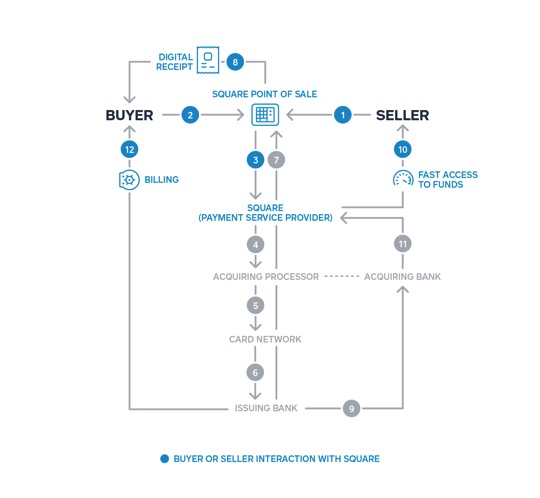

Processing card transactions requires close coordination among a number of industry participants that provide the services and infrastructure required to enable such transactions. These participants consist of payment service providers, acquiring processors, card networks, and issuing banks. Within this landscape, Square serves as a payment service provider, acting as the touch point for the seller to the rest of the payment chain. The definitions and graphic below outline this payment chain and the typical flow of a Square transaction, along with the types of fees typically paid and received at each stage.

Payment Service Provider (PSP): Provider of the payment services that holds the direct relationship with the seller and facilitates the rest of the transaction on behalf of the seller. A PSP is also the merchant of record for the transaction. The merchant of record is liable for the settlement of transactions processed and accordingly enters into contractual arrangements and negotiates terms, including pricing, with the acquiring processors and card networks. The merchant of record is also contractually responsible for settling the costs incurred in the process and is compensated by the seller for the services provided.

Acquiring Processor: Provider of the back-end technology that facilitates the flow of payment information through the Card Networks to the Issuing Bank. The company's agreements with acquiring processors typically have terms of two to four years.

Card Networks (e.g. Visa, MasterCard): Provider of the infrastructure for card payment information to flow from the Acquiring Bank to the Acquiring Processor.

Issuing Bank: The financial institution that issues the buyer’s payment card.

Acquiring Bank: The financial institution associated with the Acquiring Processor.

- Once the buyer is ready to make a purchase, the seller inputs the transaction into the Square Point of Sale and presents the buyer with the amount owed.

- For in-person transactions, the buyer pays by swiping or dipping their payment card, or by tapping their NFC-enabled payment card or mobile device on a Square Reader, Square Stand or Square Register, as applicable, which captures the buyer’s account information. For card not present transactions the seller can either use the customers' card on file or the card information is keyed in manually by either the buyer or seller into the Square Point of Sale app, Square Invoices, Square Virtual Terminal, or the seller's e-commerce website.

- The Square Point of Sale sends the transaction information to Square, which acts as the PSP.

- Square passes the transaction information to the Acquiring Processor via an internet connection. Square pays a small fixed fee per transaction to the Acquiring Processor.

- The Acquiring Processor routes the transaction to the appropriate Card Network affiliated with the buyer’s card such as Visa, Mastercard, Discover, or American Express. Square pays a variety of fees to the Card Network, the most significant of which are assessment fees that are typically less than 0.15% of the transaction amount.

- The Acquiring Processor then routes the transaction through the Card Network to the Issuing Bank, which authorizes or declines the transaction for the buyer’s payment card.

- Upon authorization, the Issuing Bank sends a notification back through the Card Network to the Square Point of Sale to inform the seller that the transaction has been successfully authorized.

- The Square Point of Sale sends a digital receipt for the transaction to the buyer, enabling a persistent communication channel between the seller and the buyer. For example, this is how the buyer can send feedback to the seller about the service provided.

- The Issuing Bank then triggers a disbursement of funds to the Acquiring Bank through the Card Network for the transaction amount. Square will ultimately pay the Issuing Bank an interchange fee as a percentage of the amount of the transaction plus a fixed fee per transaction, which together average between 1.5% to 2.0% of the transaction amount. However, this percentage can vary significantly based on the buyer's card type, transaction type, and transaction size.

- Square transfers the funds to the seller’s bank account, net of the fee charged by Square. Square provides sellers with fast access to funds, typically settling with them by the business day after the date of the transaction via Automated Clearing House (ACH) transfers, or the same day via its Instant Deposit service for an additional transaction fee. Square pays a very small fee for each ACH transfer.

- The funds are settled from the Acquiring Bank to Square, typically in one to two business days after the date of the transaction.

- At the end of each monthly billing cycle, the Issuing Bank sends a statement to the buyer showing their monthly charges. The statement includes a reference to Square as the merchant of record on the billing statement as a prefix to the seller name (denoted as SQ).

Intellectual Property

The company seek to protect its intellectual property rights by relying on a combination of federal, state, and common law rights in the United States and other countries, as well as on contractual measures. It is its practice to enter into confidentiality, non-disclosure, and invention assignment agreements with its employees and contractors, and into confidentiality and non-disclosure agreements with other third parties, in order to limit access to, and disclosure and use of, its confidential information and proprietary technology. In addition to these contractual measures, the company also rely on a combination of trademarks, trade dress, copyrights, registered domain names, trade secrets, and patent rights to help protect its brand and its other intellectual property.

Square has developed a patent program and strategy to identify, apply for, and secure patents for innovative aspects of its products, services, and technologies where appropriate. As of December 31, 2017, the company had 379 issued patents in force and 605 filed patent applications pending in the United States and in foreign jurisdictions relating to a variety of aspects of its technology. The company's issued patents in force will expire between 2032 and 2042. The company intend to file additional patent applications as the company continue to innovate through its research and development efforts and to pursue additional patent protection to the extent the company deem it beneficial and cost-effective.

The company actively pursue registration of its trademarks, logos, service marks, trade dress, and domain names in the United States and in other jurisdictions. Square is the registered holder of a variety of U.S. and international domain names that include the term “Square” and variations thereof.

From time to time, the company also incorporate certain intellectual property licensed from third parties, including under certain open source licenses. Even if any such third-party technology did not continue to be available to it on commercially reasonable terms, the company believe that alternative technologies would be available as needed in every case.

Employees

As of December 31, 2017, the company had 2,338 full-time employees. The company also engage temporary employees and consultants as needed to support its operations. None of its employees are either represented by a labor union or subject to a collective bargaining agreement. Square has not experienced any work stoppages, and the company consider its relations with its employees to be good.