TransAlta

Summary

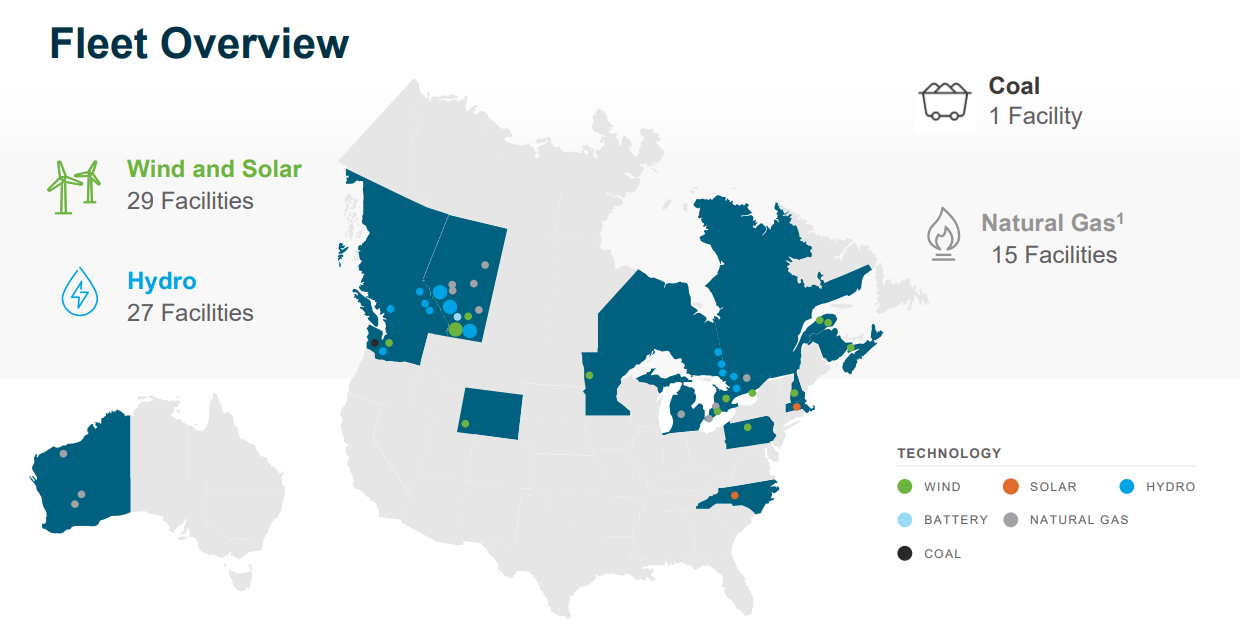

- TransAlta owns, operates and develops a diverse fleet of electrical power generation assets in Canada, the United States and Australia

- TransAlta is one of Canada’s largest producers of wind, and Alberta’s largest producer of hydroelectric power.

- TransAlta's portfolio of assets includes Solar, Wind, Hydro, Coal, Natural Gas and Energy Storage

- With more than 70 power plants in Canada, the United States and Australia, TransAlta acquired world-class development and operational expertise in generating clean power.

Company Overview

TransAlta (NYSE:TAC, TSX:TA) owns, operates and develops a diverse fleet of electrical power generation assets in Canada, the United States and Australia. As one of Canada’s largest producers of wind, and Alberta’s largest producer of hydroelectric power, the company provide clean, affordable and reliable power to its customers.1

Beginning as a small, local electricity company in 1909, TransAlta has transformed over the last century to become an experienced and well-respected electricity generator and wholesale marketer of electricity. With approximately $3 billion in annual revenue, more than $9 billion in assets and operations in three countries, TransAlta has proven its worth as an electricity producer, as a community member and as a solid investment.

Company History

Since 1911, TransAlta has supplied the electrical power needed to make progress and innovation possible in Alberta – and beyond.2

In the beginning, its growth was tied to the evolution of a province steeped in prairie optimism and rich natural resources. More recently, we’ve powered industry, commerce and community well-being across Canada, in the U.S. and Australia.

| Year | Milestones |

| 1909 - 1919 | When the province of Alberta was four years old, the company began its journey with the planning and construction of the Horseshoe Falls Hydro Plant. Two years later, with the help of 200 workers, the company flipped the switch and Calgary Power Company Ltd. was born. The company's second dam was commissioned in 1913 at Kananaskis Falls, built by almost 500 workers. |

| 1920 - 1929 | Electricity was being put to new uses – from powering street lamps to motion pictures – all while contributing to the exploration and early economic success of Alberta. |

| Electricity transformed daily life at home, on the farm and at work with the introduction of water pumps, refrigerators, milking machines and stoves. | |

| 1930 - 1939 | Fortunately, the company were strong enough to continue operations when the Great Depression hit without having to lay off a single employee. |

1940 - 1949 | |

| With the onset of the Second World War, many employees enlisted to serve their country. In 1941, the company began assigning employee numbers and Jal Abelseth of the Seebe plant was honoured with being one employee. | |

| 1950 - 1959 | By 1950, the company had more than 400 staff members and offices across Alberta, including: Edmonton, Camrose, Wetaskiwin, Calgary and Lethbridge. In addition, the company served 6,000 new customers and 24 additional towns and villages. |

| 1960 - 1969 | 1961 marked its first 50 years of operation and Calgary Power reached an agreement with the Alberta government to jointly construct a multi-use dam on the Brazeau River, including a storage dam that was constructed on the North Saskatchewan River. The first turbine was commissioned in 1965. |

| 1970 - 1979 | By the early ’70s, society was becoming environmentally conscious. The company responded by retrofitting boilers with electrostatic precipitators which removed 99.5 per cent of fly ash from emissions. While interest rates rose, the company continued to expand to keep up with the needs of a growing province. |

| 1980 - 1989 | In 1981, the company officially changed its name and became TransAlta, the new name better reflecting its now province-wide operations, having expanded to supply 81 per cent of Alberta’s electrical requirements by the end of the decade. |

| 1990 - 1999 | In the ’90s, TransAlta worked with government to define the open, competitive and deregulated electricity market that would come about in the new millennium. |

| Through the 1990s, the company learned a great deal about competing internationally and in newly deregulated markets by operating hydroelectric facilities in Argentina, as well as power plants in Australia and New Zealand. | |

| 2000 - 2009 | With deregulation now in effect, TransAlta became the first Canadian electrical generation company to be listed on the New York Stock Exchange. The company has since grown to become the largest investor-owned generator of renewable energy in Canada. |

| 2010 and Beyond | Since 2009, TransAlta has focused on increasing investment in a diversified generation fleet of low-cost power assets that serve customers in the various cities, regions and countries the company operate in. Today, TransAlta is one of Canada’s largest wind operators, Alberta’s largest hydro operator and have diversified its generation mix to include sources such as solar. |

Operations

The company's growing portfolio of assets powered by Solar, Wind, Hydro, Coal, Natural Gas and Energy Storage are necessary to maintain a healthy and stable electricity supply. With more than 70 power plants in Canada, the United States and Australia, TransAlta acquired world-class development and operational expertise in generating clean power.

| As at Dec. 31, 2021 | Hydro | Wind and Solar | Gas | Energy Transition | Total | |

| Alberta | Gross installed capacity (MW)(1) Number of facilities Weighted average contract life(2) | 834 17 — | 636 13 7 | 1,960 7 1 | 801 2 — | 4,231 39 2 |

| Canada, Excl. Alberta | Gross installed capacity (MW)(1) Number of facilities Weighted average contract life(3) | 91 9 7 | 751 9 10 | 645 3 6 | — — — | 1,487 21 8 |

| US | Gross installed capacity (MW)(1) Number of facilities Weighted average contract life(3) | — — — | 519 7 12 | 29 1 4 | 671 2 4 | 1,219 10 8 |

| Australia | Gross installed capacity (MW)(1) Number of facilities Weighted average contract life(3) | — — — | — — — | 450 6 17 | — — — | 450 6 17 |

| Total | Gross installed capacity (MW)(1) Number of facilities Weighted average contract life(3) | 925 26 1 | 1,906 29 9 | 3,084 17 5 | 1,472 4 2 | 7,387 76 5 |

The company's Clean Energy Investment Plan, announced in 2019, included converting its existing Alberta coal assets to natural gas and advancing its leadership position in renewable electricity. To date, TransAlta has retired 4,064 MW of coal-fired generation capacity since 2018 while converting 1,659 MW to natural gas, significantly reducing its carbon footprint. During 2021, the company increased its renewable fleet by 334 MW through acquisitions and construction of renewable wind and solar facilities and on Sept 28, 2021, the company announced a Clean Electricity Growth Plan that includes strategic growth targets. Please refer to the Accelerated Clean Electricity Growth Plan section of this MD&A for further information.3

Approximately 57 per cent of its gross installed capacity is located in Alberta. The company's portfolio of merchant assets in Alberta is a combination of hydro facilities, wind facilities, a battery storage facility and converted natural-gas-fired thermal facilities. This balance of fuel types provides it with portfolio generation diversification. It also provides it with capacity that can be monetized as ancillary services or dispatched into the energy market during times of supply tightness. The company also enter into financial contracts to reduce its exposure to variable power prices on its merchant generation. Please refer to the Alberta Electricity Portfolio section of this MD&A for further information.

Financial Highlights

Adjusted availability for 2021 was 86.6 per cent compared to 90.7 per cent in 2020. The decrease was primarily due to higher planned and unplanned outages in the Energy Transition segment. The unplanned outages at Centralia Unit 2 and Sundance Unit 4 adversely impacted availability. In addition, adjusted availability was reduced by the planned outages for the Keephills Unit 2 and Keephills Unit 3 boiler conversions. The unplanned outage at the Kent Hills 1 and 2 wind facilities further contributed to reduced adjusted availability.

Production for 2021 was 22,105 gigawatt hours ("GWh") compared to 24,980 GWh in 2020. Overall, the decrease in production was primarily due to the planned retirement of Centralia Unit 1, portfolio optimization activities in Alberta, lower wind resources, the outage at the Kent Hills 1 and 2 wind facilities in the Wind and Solar segment and lower capacity loads in the Gas segment. This was partially offset by higher incremental production at its Ada facility within its Gas segment and higher incremental production from the Skookumchuck wind facility, the Windrise wind facility and the North Carolina Solar facility in the Wind and Solar segment.

Revenues for 2021 increased by $620 million compared to 2020, mainly as a result of capturing higher realized prices within the Alberta market through its optimization and operating activities and the elimination of the net payment obligations under the Alberta Hydro PPA required in the prior period. Revenues also increased due to the strong performance from the Energy Marketing segment, an increase in revenues within the Gas segment from the addition of the Ada facility and an increase within the Wind and Solar segment from the addition of the North Carolina Solar facility and the Windrise wind facility. These increases were partially offset by lower production in the Energy Transition, Hydro, Wind and Solar, and Gas segments.

Fuel and purchased power costs in 2021 increased by $249 million compared to 2020. In its Energy Transition segment, its fuel and purchased power costs increased compared to 2020 due to higher fuel transportation costs and the acquisition of higher-priced power during periods of higher merchant pricing to fulfil its contractual obligations during planned and unplanned outages at the Centralia facility. In addition, the Gas and Energy Transition segments experienced higher natural gas pricing, higher coal mine depreciation and coal inventory write-downs at the Highvale mine, all of which contributed to higher fuel costs.

Carbon compliance costs increased by $15 million compared to 2020, due to an increase in the carbon price per tonne, partially offset by reductions in GHG emissions stemming from changes in the fuel mix ratio as the company operated more on natural gas and fired less with coal. Additionally, carbon compliance costs were partially offset by lower production in the Gas and Energy Transition segments. Operating with natural gas reduces carbon compliance costs as the company produce fewer GHG emissions than by using coal.

Operations, maintenance and administration ("OM&A") expenses for 2021 increased by $39 million compared to 2020. A write-down of $28 million was recorded on parts and material inventory related to the Highvale mine and coal operations at its natural gas converted facilities. In addition, variability caused by the total return swap resulted in a favourable change of $7 million. During 2021, the company received a Canada Emergency Wage Subsidy ("CEWS") of $8 million. Excluding the impact of the total return swap, CEWS funding and inventory write-down, OM&A expenses were higher compared to the same periods in 2020, primarily due to increased staffing costs for growth and strategic initiatives and higher incentive costs. In addition, there were additional costs associated with the legal fees and the settlement of outstanding legal issues. As previously committed, the CEWS funding continues to be used to support incremental employment within the Company.

Adjusted EBITDA increased by $336 million compared to 2020. Adjusted EBITDA increased largely due to higher gross margin, driven by higher realized prices and dispatch optimization in the Alberta market from its merchant facilities residing in the Alberta Electricity Portfolio across the Hydro, Wind and Solar, Gas, and Energy Transition segments. In addition, the Energy Marketing segment also increased adjusted EBITDA due to favourable short-term trading of both physical and financial power and natural gas products across North American markets. This increase was partially offset by the retirement of Centralia Unit 1, unplanned outages at Centralia Unit 2 in the Energy Transition segment and the extended site outage at the Kent Hills 1 and 2 wind facilities.

Loss before income taxes for 2021 increased by $77 million compared to 2020. Net loss attributable to common shareholders for 2021 was $576 million compared to a loss of $336 million in 2020. The higher loss before income taxes and the higher net loss attributable to common shareholders in 2021 was largely driven by higher asset impairments related to decisions to shut down the Highvale mine, suspend the Sundance 5 repowering project and planned retirements of Sundance Unit 4 and Keephills Unit 1. These higher asset impairments were partially offset by higher adjusted EBITDA largely resulting from the strong performance of the Alberta Electricity Portfolio across all of its fuel segments, higher gains on sale of assets due to the gain on sale of equipment in the Energy Transition segment and the gain from the sale of the Pioneer Pipeline in the Gas segment and lower depreciation. The higher net loss attributable to common shareholders was also impacted by higher income tax expense in 2021 due to higher earnings in the Energy Marketing segment and from the Alberta Electricity Portfolio.

Cash flow from operating activities increased by $299 million compared with 2020, primarily due to higher revenues being realized in Alberta on the merchant assets and changes in non-cash working capital, partially offset by higher fuel and purchased power and OM&A costs as the Company transitioned off coal.

FCF, one of the Company's key financial metrics, totalled $562 million compared to $358 million in 2020. This represents an increase of $204 million, driven primarily by higher adjusted EBITDA, partially offset by an increase in sustaining capital spending related to higher planned maintenance and facility turnarounds, settlement of provisions and higher distributions paid to subsidiaries' non-controlling interests.

First Quarter 2022 Results

May 6, 2022; TransAlta reported its financial results for the first quarter ended March 31, 2022.4

“TransAlta delivered solid first quarter results for 2022 with contributions from its new contracted assets at Windrise and North Carolina Solar which diversified its portfolio. I am also pleased to confirm that TransAlta is on track to deliver its objectives under its Clean Electricity Growth Plan,” said John Kousinioris, President and Chief Executive Officer.

“The company delivered growth in renewable energy to new and existing customers in all three core geographies of its operations. The company reached final investment decision on its 200 MW Horizon Hill project in Oklahoma by signing a long-term PPA with Meta. The company fully contracted its Garden Plain facility by adding another long-term PPA for the remaining 30 MW of capacity with an investment-grade globally recognized customer. And in Western Australia, the company reached final investment decision on the Mount Keith transmission expansion project which will enable the connection of additional generating capacity to its network and will support BHP’s operations and increase their competitiveness as a supplier of low-carbon nickel.”

Adjusted EBITDA for the three months ended March 31, 2022 was $266 million, a decrease of $44 million, or 14% per cent compared to the same period in 2021, largely due to lower adjusted EBITDA at its Gas, Energy Transition, Hydro, and Energy Marketing segments and higher corporate costs. This was partially offset by higher adjusted EBITDA at its Wind and Solar segment.

Earnings before income taxes for the three months ended March 31, 2022 increased by $221 million compared to the same period in 2021. Net earnings attributable to common shareholders for the three months ended March 31, 2022 was $186 million compared to a net loss of $30 million in the same period of 2021, an improvement of $216 million. The increase in earnings before income taxes and net earnings attributable to common shareholders in 2022 was largely driven by higher revenues from the Alberta Electricity Portfolio, lower carbon compliance costs and lower depreciation, mainly as a result of the completion of its coal-to-gas conversions and retirement of its coal assets compared to the same period in 2021. In addition, an asset impairment reversal driven by discount rate changes was recognized in 2022 compared to impairment charges in 2021. The higher net earnings attributable to common shareholders was also impacted by higher income tax recoveries in 2022.

Cash flow from operating activities for the three months ended March 31, 2022 was $451 million, an increase of $194 million compared with the same period of 2021, primarily due to favourable changes in non-cash working capital and higher revenue attributable to the North American Gas assets, converted gas units and higher revenues in the Wind and Solar segment as well as lower fuel and purchased power and carbon compliance costs as the Company transitioned its units to natural gas.

FCF for the three months ended March 31, 2022, was $115 million, a decrease of $14 million compared with the same period of 2021, driven primarily by lower adjusted EBITDA, higher distributions paid to subsidiaries’ non-controlling interests, partially offset by a decrease in sustaining capital spending related to lower planned maintenance turnarounds.

Key Business Developments

200 MW Horizon Hill Wind Project and Fully Executed Corporate PPA with Meta

On April 5, 2022, TransAlta executed a long-term PPA with a subsidiary of Meta Platforms Inc., formerly known as Facebook, Inc. (“Meta”), for 100 per cent of the generation from its 200 MW Horizon Hill wind project to be located in Logan County, Oklahoma. Under this agreement, Meta will receive both renewable electricity and environmental attributes. The facility will consist of a total of 34 Vestas turbines with construction expected to begin in late 2022 and a target commercial operation date in the second half of 2023. TransAlta will construct, operate and own the facility. Total construction capital is estimated at approximately US$290 million to US$310 million and is expected to be financed with a combination of existing liquidity and tax equity financing. Over 90 per cent of project costs are captured under executed turbine supply agreements and engineering, procurement and construction agreements. The project is expected to generate average annual EBITDA of approximately US$27 million to US$30 million inclusive of production tax credits.

Executed Long Term PPA for Remaining 30 MW at Garden Plain

The Company has entered into a long-term PPA for the remaining 30 MW of renewable electricity and environmental attributes at the Garden Plain wind farm in Alberta with a new investment-grade globally recognized customer. The 130 MW Garden Plain wind project, which was announced in May 2021 with a 100 MW PPA with Pembina Pipeline Corporation, is now fully contracted with a weighted average contract life of approximately 17 years. Construction is underway with a target commercial operation date in the second half of 2022.

Mt. Keith Transmission Expansion

On May 3, 2022, TransAlta Renewables exercised its option to acquire an economic interest in the expansion of the Mt. Keith 132kV transmission system in Western Australia, to support the Northern Goldfields-based operations of BHP Nickel West (“BHP”). Total construction capital is estimated at approximately AU$50 million to AU$53 million. Southern Cross Energy, a subsidiary of the Company, has entered into an engineering, procurement and construction agreement with ASX-listed GenusPlus Group Ltd for the expansion. The project is being developed under the existing PPA with BHP, which has a term of 15 years. It is expected to be completed in the second half of 2023 and will generate annual EBITDA in the range of AU$6 million to AU$7 million. In addition, the planned completion date should allow at least a portion of the project to qualify for Australia’s “Temporary Full Expensing” COVID-19 tax benefit. The project will facilitate the connection of additional generating capacity to its network to support BHP’s operations and increase their competitiveness as a supplier of low-carbon nickel.

Sarnia Cogeneration Facility Contract Extensions

The Company recently entered into agreements with three of its large industrial customers at the Sarnia cogeneration facility. The capacity commitments for the large industrial customers have now been extended to 2031, at rates comparable to current contract rates, which, in each case, are subject to the satisfaction of certain conditions, including the Company entering into a new contract with the Ontario Independent Electricity System Operator (the “IESO”). The IESO is conducting a medium-term procurement process for capacity for 2026 and beyond for existing generation. The Company has bid into the process, and is seeking to secure a contract extension for the Sarnia cogeneration facility following the end of the current IESO contract expiring on Dec. 31, 2025. The Company expects the IESO to announce the successful bids in the third quarter of 2022.

Kent Hills Wind Facilities Rehabilitation Progress

During the first quarter of 2022, the extended outage at Kent Hills 1 and 2 wind facilities continued. Rehabilitation efforts for the foundations are expected to commence during the second quarter of 2022 with the aim of fully returning the wind facility to service during the second half of 2023.

References

- ^ https://www.transalta.com

- ^ https://www.transalta.com/about-transalta/history/

- ^ https://fintel.io/doc/sec-travelcenters-of-america-inc-md-1378453-10k-2022-february-23-19046-4863

- ^ https://transalta.com/newsroom/news-releases/transalta-reports-first-quarter-results-and-reaches-40-of-renewables-growth-target/