Muthoot Finance Ltd

Summary

- The Muthoot Group began started in 1887 in the remote village of Kozhencherry in Kerala.

- Over the past 133 years, the Group has grown as many as 20 business divisions and 5,300+ branches.

- Muthoot Finance is country’s largest gold financing company.

Company Overview

The Muthoot Group began its journey in 1887 in the remote village of Kozhencherry in Kerala. It was founded as a modest trading business in a region that was geographically disadvantaged and lacking in mobility, land, resources, industry or favourable market conditions. Over the past 133 years, the Group has grown into a flourishing conglomerate, reaching out into India’s small and large towns as well as its major cities through as many as 20 business divisions and 5,300+ branches. 1

Muthoot Finance Limited (Muthoot Finance) is the flagship business of the Muthoot Group and India’s largest gold financing company. It is registered as a ‘Systemically Important Non-Deposit-Taking Non-Banking Financial Company (NBFC-ND-SI)’ with the Reserve Bank of India (RBI).

Shri M. George Muthoot, the son of Shri Ninan Mathai Muthoot, founded the gold loan business in 1939. Today, Muthoot Finance has evolved into one of India's most trusted financial services brands and the country’s largest gold financing company (by loan portfolio).

The company primarily provide business loans secured by gold jewellery (or gold loans) and cater to individuals who possess gold jewellery but cannot access formal credit within a reasonable time, or for whom credit may not be available at all.

The company spent the last few years putting in place a rock-solid foundation of core systems, which the company can build upon to augment its productivity, accelerate product and service innovations, and deliver a seamless digital customer experience across multiple touchpoints.

Milestones

| 1887 | The Group commenced its journey as a trading business in a village in Kerala |

| 1939 | Muthoot Finance commenced gold loan business |

| 2001 | Received the RBI licence to function as an NBFC |

| 2010 | Branch network crossed 1,600 |

| 2012 | Successful IPO of `9,012.50 millions in April 2011 |

| 2015 | Acquired 51% of capital of Asia Asset Finance Plc, making it a subsidiary |

| 2016 | Acquired Muthoot Insurance Brokers Private Limited as a wholly-owned subsidiary |

| 2019 | Incorporated Muthoot Asset Management Private Limited and Muthoot Trustee Private Limited as wholly-owned subsidiaries |

Product and Services

- Gold Loan

- Housing Finance

- Personal Loan

- Insurance

- Gold Coin

- Money Transfer

- Foreign Exchange

- NCD

- Mutual Funds

- Muthoot iWill

- PAN Card

- Micro Finance

- Digital & Cashless

- Vehicle Loan

- Loan@Home

- Corporate Loan

- SME Loan

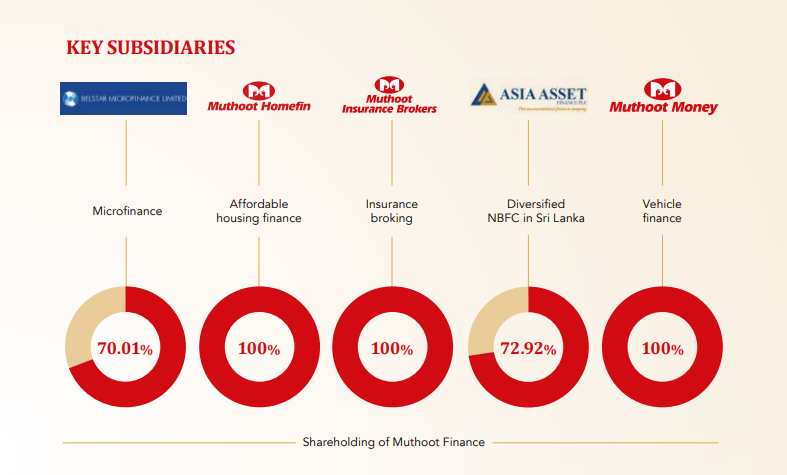

Belstar Microfinance Limited

Belstar Microfinance Limited was incorporated in January 1988 in Bengaluru and registered with the RBI in March 2001 as an NBFC. The company was reclassified as an ‘NBFC-MFI’ by the RBI effective December 11, 2013, and provides scalable microfinance services to entrepreneurs following the Self-Help Group (SHG) model.

Muthoot Homefin (India) Limited

Muthoot Homefin (India) Limited is a housing finance company registered with the National Housing Bank (NHB). Incorporated in 2011, it became a wholly-owned subsidiary of Muthoot Finance in August 2017.

The company focuses on extending affordable housing finance and targets customers in Economically Weaker Sections (EWS) and Lower Income Groups (LIG) in Tier II and Tier III locations. It operates on a hub-and-spoke model, with a presence in 16 states and centralised processing at the Corporate Office in Mumbai.

Asia Asset Finance Plc

Asia Asset Finance Plc, Colombo, Sri Lanka became a foreign subsidiary of Muthoot Finance on December 31, 2014. It is a fully licensed, deposit-taking institution registered with the Central Bank of Sri Lanka and listed in the Colombo Stock Exchange; and has been in the lending business since 1970. Formerly known as Finance and Land Sales, it has evolved to serve the growing needs of the people of Sri Lanka.

Through a widespread branch network, the company has operations in various parts of Sri Lanka, providing the best services and easy access to clients. By 2025, Asia Asset Finance Plc aims to become the leading gold loan company in Sri Lanka.

Muthoot Insurance Brokers Private Limited

Muthoot Insurance Brokers Private Limited became a wholly-owned subsidiary of Muthoot Finance in September 2016. It is an unlisted private limited company holding a licence to act as Direct Broker from the Insurance Regulatory and Development Authority since 2013. It is actively distributing both life and non-life insurance products of various insurance companies.

Muthoot Money Limited

Muthoot Money Limited became a wholly-owned subsidiary of Muthoot Finance in October 2018. The company is an RBI registered NBFC engaged mainly in the financing of used and new commercial vehicles, passenger vehicles, construction equipment, and other asset finance solutions. Further, CRISIL assigned longterm debt rating of CRISIL AA-/Positive for bank limits.

Industry Overview

NBFCs

NBFCs deliver credit to a wide variety of niche segments, ranging from infrastructure to consumer durables, and have always played a vital role in emerging economies like in India, where they catalyse financial inclusion by reaching out to the underserved segments and supplementing the role of banks.

In the last two years, the non-banking sector underwent significant turbulence on account of a few beleaguered NBFCs like Dewan Housing and Finance (DHFL), Infrastructure Leasing & Financial Services (IL&FS), etc. During this time, the liability profile of NBFCs changed gradually as they recorded a rise in the share of borrowings from banks vis-à-vis market instruments.

Fresh concerns around asset quality emerged in FY20, owing to the slowdown in the auto and real estate sectors and subdued consumer demand. In response, most NBFCs focused on reducing exposure to low-margin businesses to maintain spreads and adopting a cautious approach to lending – choosing to shore up liquidity instead. The Government and the RBI instituted measures to strengthen governance and risk management frameworks of NBFCs and put in place various channels for the companies to raise funds.

Gold

As a store of value and as an article inexorably linked to human emotions through generations of social conditioning and collective memory, gold has carved its unique place in the Indian economy. Gold is rarely ever sold, but often pledged to obtain loans, particularly in rural areas, where bank penetration is limited and there is seasonal demand for ready cash that is met increasingly by the NBFCs, who have driven the trade from the clutches of moneylenders to more formal financial channels. More than two-thirds of India’s demand for gold loans is said to emanate from rural communities.

Specialised gold loan NBFCs like Muthoot Finance occupy a niche in the gold financing business through proactive marketing, sustained geographic expansion, higher branch productivity and strong customer relations.

Jewellery demand

India is one of the largest markets for gold and growing affluence is driving growth in its demand. In the April-June quarter of 2019, Indian jewellery demand gained 12%, to 168.6 tonnes, as compared to 149.9 tonnes in the previous year, largely due to two factors: a higher number of auspicious wedding days compared to 2018 and local gold prices moving lower from the levels seen in February and March 2019. By September, the jewellery demand fell 32% to 101.6 tonnes, on the back of weakened consumer sentiment. The trend continued in the October-December quarter, generating a 17% decline amidst record high gold price levels, domestic economic slowdown and muted rural demand. Weddings and retailer promotions checked the downfall to some extent, but volumes were soft compared to the previous year.

Investment

Of all precious metals, gold is the most popular as investment. Some of the most notable gold investment products include gold-backed Exchange-Traded Funds (ETFs) and official gold bars and coins. Seen as measure of creditworthiness, cultural and material legacy and social status, gold virtually carries its own weight in India.

In the January-March quarter of 2020, bar and coin investment in India fell 17% y-o-y to 28 tonnes – its lowest level for four years. Having fallen prey to volatile local gold prices in January and February, the lockdown imposed in March effectively brought retail investment to a halt. Availability of bars and coins became problematic after the closure of retail shops and bullion dealers. However, interest in digital gold products continued to grow during this time, as it became easier to buy gold via such platforms. This echoed the rise in demand for ETFs in India, which saw relatively sizeable inflows of 4.4 tonnes as fears over the social and economic impact of the virus drove safe-haven flows into gold investment products globally.

Organised gold loan market

The organised sector comprising banks (public, private, small finance and co-operative), NBFCs and Nidhi companies contribute to nearly 35% of the market.7 With more financial institutions increasing their geographic scope and market penetration, a large portion of the underbanked population, who historically relied on lenders within the unorganised sector to fund their needs, is crossing over to the organized sector. This has brought them into the fold of the formal credit system and helped create credit records for the first time, thereby enabling them to obtain loans from organised credit institutions. Against this backdrop, specialised gold loan NBFCs are poised to capture a large share of the customers shifting to the organised sector.

Financial Overview

Muthoot Finance is revolutionising India’s gold banking sector and empowering people across the social pyramid. Inspired by a rich legacy that goes back several generations, its team of 25,000+ employees serve 200,000+ customers every day, through 4,500+ branches, the majority of which are in semiurban and rural India.

The company's consolidated loan assets under management for FY20 stood at Rs 468,705 millions as against Rs 383,036 millions last year, registering a year-on-year increase of 22%.

The company's total gold loan outstanding was Rs 407,724 millions in FY20, up 21% from Rs 335,853 millions the previous year. The average gold loan per branch was Rs 89.28 millions in FY20, up 19% from Rs 74.97 millions last year.

The company's total income grew from Rs 76,010 millions in FY19 to Rs 97,072 millions in FY20, registering a year-on-year increase of 28%.

Profit before tax was Rs 42,604 millions in FY20, against Rs 32,595 millions last year.

Profit after tax achieved a year-on-year increase of 51% and stood at Rs 31,687 millions in FY20 vis-à-vis Rs 21,030 millions the previous year.

The capital adequacy ratio stood at 25.47% in FY20 with a Tier I capital of 24.30% and Tier II capital of 1.17%.

Earnings per share increased to Rs 78.30 in FY20 from Rs 51.92 in the previous year.

March 2021 Result

June 03, 2021; Reported Consolidated quarterly numbers for Muthoot Finance are: 2

Net Sales at Rs 3,104.50 crore in March 2021 up 18.02% from Rs. 2,630.50 crore in March 2020.

Quarterly Net Profit at Rs. 1,019.97 crore in March 2021 up 22.98% from Rs. 829.37 crore in March 2020.

EBITDA stands at Rs. 2,456.56 crore in March 2021 up 22.25% from Rs. 2,009.42 crore in March 2020.

Muthoot Finance EPS has increased to Rs. 25.42 in March 2021 from Rs. 20.68 in March 2020.