Piramal Enterprises Ltd

Summary

- Piramal Group is a global business conglomerate with diverse interests in Pharma, Financial Services and Real Estate.

- The Group has offices in over 30 countries and a global brand presence in more than 100 markets.

- In October 2020, the company raised fresh equity from The Carlyle Group for a 20% stake in Piramal Pharma.

Company Overview

Piramal Group is a global business conglomerate with diverse interests in Pharma, Financial Services and Real Estate. The Group has offices in over 30 countries and a global brand presence in more than 100 markets.1

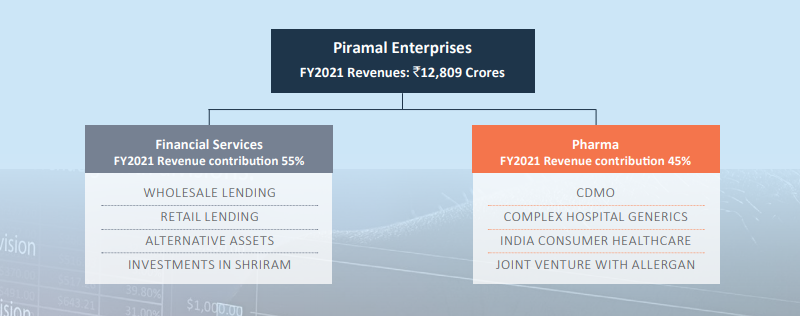

Piramal Enterprises Limited (NSE: PEL) is one of India’s leading diversified companies, with a presence in Financial Services and Pharmaceuticals. PEL’s consolidated revenues were ~US$1.7 Billion in FY2021, with around ~37% of revenues generated from outside India. Driven by both organic as well as inorganic strategy, PEL has steered dynamic business growth over the three decades of its existence.

Financial Services

The Company offers a wide range of financial products and solutions, with presence across both retail and wholesale financing. As of March 31, 2021, the Financial Services business had loan book of Rs 44,668 Crore.

Within retail lending, the Company is building a multi-product platform and offers home loans, loans for small businesses and loans for working capital to customers in affordable housing and mass affluent segments across Tier I, II and III cities. The business is ‘digital at the core’ and its modular structure has the ability to add multiple products such as loans for two-wheelers, education and purchase finance. The Company is in the process of acquiring Dewan Housing Finance Corporation Limited (DHFL). The acquisition of DHFL fits well into the Company’s strategy to diversify the loan book and helps achieve scale its Retail lending business.

Within wholesale lending, the business provides financing to real estate developers, as well as corporate clients. The real estate platform provides financing solutions to developers, which includes Construction Finance. In Corporate Lending, the business provides customised funding solutions to companies across non-real estate sectors, such as infrastructure, renewable energy, auto components etc.

The Company has also formed strategic partnerships with leading financial institutions such as CPPIB, APG and Ivanhoe Cambridge, etc. across various investment platforms. It has built a Distressed Asset Investing platform with Bain Capital Credit (IndiaRF) which invests in equity and/or debt across non-real estate sectors. PEL also has equity investments in Shriram Group, a leading financial conglomerate in India.

Pharma

PEL has a differentiated business model that is diversified across three segments: Contract Development and Manufacturing Organization (CDMO), Complex Hospital Generics (CHG) and India Consumer Healthcare. Through endto-end manufacturing capabilities across 14 global facilities and a large global distribution network spanning over 100 countries, PEL sells a portfolio of niche differentiated pharma products and provides an entire pool of pharma services.

PEL’s CDMO business offers integrated solutions across the drug lifecycle - ranging from discovery clinical development to commercial manufacturing of Active Pharmaceutical Ingredients (APIs) and Formulations. The Complex Hospital Generics business markets niche inhalation anaesthesia, injectable anaesthesia, intrathecal spasticity and pain management and select antibiotics. PEL’s Consumer Healthcare business is among the leading players in India in the self-care space, with established brands in the Indian consumer healthcare market. The Pharma Business has a joint venture with Allergan, a leader in ophthalmology in the Indian formulations market.

In October 2020, the company raised fresh equity from The Carlyle Group for a 20% stake in Piramal Pharma.

Plant Locations

Plant Locations of the Company (PEL) and its Subsidiaries

India

PEL

- Raigad, Maharashtra

Piramal Pharma Limited

- Dhar, Madhya Pradesh

- Zaheerabad, Telangana

- Chennai, Tamil Nadu

- Ahmedabad, Gujarat

Convergence Chemicals Private Limited

- Dahej, Tal Vagra, Gujarat

Overseas

Piramal Healthcare UK Limited

- Northumberland, UK

- Scotland, UK

Piramal Healthcare (Canada) Limited

- Aurora, Ontario, Canada

iramal Critical Care Inc.

- Brodhead Road, USA

Piramal Pharma Solutions Inc.

- Kentucky, USA

Ash Stevens LLC

- Krause Street, Riverview, USA

PEL Healthcare LLC

- Sellersville, USA

Business Overview

Financial Services

PEL's Financial Services offers a wide range of financial products and solutions with presence across both retail and wholesale financing. As of March 31, 2021, the Financial Services business’s loan book stood at Rs 44,668 Crore. 2

Market Scenario – Financial Services

The Indian economy witnessed contraction in FY2021. This was characterised by a slowdown in corporate and public revenues, increased unemployment and low demand. Fortunately, timely expansionary monetary policies ensured abundant liquidity supporting India’s financial system.

Non-Banking Financial Companies (NBFCs) reported healthy loan book growth of 18% CAGR1 between FY2014 to FY2018. However, the sector began facing prolonged macroeconomic uncertainty due to a succession of events including: liquidity tightening (since September 2018) post IL&FS crisis, slowdown in GDP growth in FY2019 & 2020 and the ongoing COVID-19 pandemic beginning March 2020. Consequently, the NBFC sector witnessed moderate growth in recent years with some companies seeing a reduction in their loan book or assets under management (AUM).

While the second wave of COVID-19 aggravated the existing uncertainty in the NBFC sector, its impact is expected to be limited. Stronger NBFCs are relatively better placed now to deal with the second wave of COVID-19, as they have improved the resilience of their balance sheet and the deterioration in asset quality remains limited, given sectors such as real estate construction, infrastructure, mining, etc. continue to remain operational.

Going forward, the ‘retailisation’ trend across NBFCs is expected to gain ground. Also, NBFCs are increasingly leveraging co-lending and partnerships to drive growth, while focusing on strengthening asset quality and tightening underwriting standards. With Indian consumers going digital at an unprecedented pace, ‘digitisation’ across the customer life cycle is likely to increase significantly. NBFCs with strong parentage will continue to have better access to funding. Moreover, the sector will continue to witness consolidation as NBFCs with strong capital base, low leverage and high on-balance sheet liquidity will continue to gain market share.

Retail Lending

Lending to consumers and micro, small and medium-scale enterprises (MSMEs) is a large business in India. The market size1 was estimated to reach Rs 96 lakh Crore in FY2024 from `48 lakh Crore in FY2019. However, retail credit growth was impacted due to lockdowns amid the COVID-19 pandemic.

Since retail lending penetration2 in India is relatively low and stood at 12% of the country’s GDP compared to ~55% in China and 76% in the US in 2020, the market offers significant long-term growth potential. The last two decades witnessed a significant increase in credit activity in rural and semi-urban markets.

Within retail lending, housing finance forms a sizable portion of the loans outstanding. Historically, home loan disbursements witnessed healthy growth owing to the increasing demand from Tier-II and -III cities, growing disposable incomes, government initiatives and fiscal incentives. Going forward, mid-town India (‘Bharat’) is expected to drive the growth in consumer and MSME credit.

Some NBFCs/HFCs were instrumental in providing retail credit to these markets owing to their deep understanding of target customer segments, use of technology and differentiated business models. Since September 2018, which spelt the beginning of liquidity tightening measures in the NBFC sector, several players limited their credit exposure to these markets or completely vacated this space.

When the economy was impacted by the COVID-19 pandemic in 2020, NBFCs/HFCs maintained a cautious stance towards loan disbursements during the lockdown period. While there was a gradual increase in growth momentum and an improvement in collections from October 2020 onwards, the second wave of COVID-19 partially reversed these recovery gains.

The current market dislocation caused by the pandemic has created several opportunities for new entrants and incumbents to capture the market vacated by a few larger NBFCs. With adequate growth capital, robust risk management and “next-gen” tech capabilities, NBFCs/HFCs are well-positioned to tap this opportunity and meet the evolving needs of the customers.

During FY2021, the business was largely focused on secured lending, while testing volumes of unsecured products, given the impact of COVID-19 on retail credit growth and consumer behaviour. In the near term, the business intends to remain largely secured-focused. Additionally, PEL is evaluating products in the space of education financing, unsecured business lending, loans against securities and two-wheeler financing. Post evaluation, some of these products will be rolled-out in the near-to-medium term.

Proposed DHFL acquisition

The Reserve Bank of India (RBI) had referred DHFL to the National Company Law Tribunal (NCLT) in November 2019, following which the insolvency proceedings began. The Committee of Creditors’ (CoC) voting ended in January 2021 and the CoC declared the plan submitted by Piramal Capital & Housing Finance Limited as the successful resolution plan. Piramal’s resolution plan received 94% votes in its favour, which reflects the Group’s credibility and balance sheet strength.

For the acquisition of DHFL, the Company offered a total consideration of `34,250 Crore. This amount includes an upfront cash component of `14,700 Crore (including cash on DHFL’s balance sheet) and a deferred component (NCDs) of `19,550 Crore.

Wholesale Lending

The year FY2021 was unprecedented for the Indian real-estate market due to the impact of the COVID-19 pandemic during the first half, followed by resurgence of demand in the latter part of the year. The broad-based disruption caused by the pandemic weighed heavily on the sector’s demand and supply in Q1 FY2021. However, after the first few months of FY2021, the company saw increase in demand from home buyers, led by change in preference towards owning homes/owning larger homes instead of renting. This trend along with decade-low home loan interest rates, price correction or discounts offered by developers and the stamp duty cuts introduced by state governments (especially Maharashtra) led to significant increase in demand during H2 FY2021. As a result, sector-wide residential realestate sales volumes steadily improved since Oct-2020, surpassing pre-COVID levels during H2 FY21.

The resurgence of COVID-19 since mid-March 2021 followed by mobility restrictions and lockdown challenges impacted the realestate sector in the near term. With mobility restrictions being lifted in some states, positive long-term economic outlook and the preparedness of the sector to mitigate risks, India’s realestate sector is likely to witness healthy growth in the long-term. Presently contributing 6-7% to the country’s GDP, real estate in India is expected to contribute 13% to the GDP by 2025, according to estimates by India Brand Equity Foundation (IBEF).

Going forward, the progress of the vaccination drive in the country and the government’s stance on restrictions will be the key influencers of the sector’s performance in the near term. Moreover, the pandemic is likely to further accelerate the pace of the on-going consolidation in the sector.

In line with the Company’s stated strategy, the overall loan book reduced from Rs 50,963 Crore as of March 2020 to Rs44,668 Crore as of March 2021. FY2021 revenues of Financial Services were impacted, primarily due to a reduction in the wholesale loan book. Revenues declined 8% yoy from `7,649 Crore in FY2020 to Rs 7,033 Crore in FY2021. Further, the business reported a post-tax return on equity (ROE) of 10% for FY2021 as compared to 12.4% (on a normalised basis) for FY2020, amidst a fall in revenues and an increase in the equity base during the year.

PHARMA

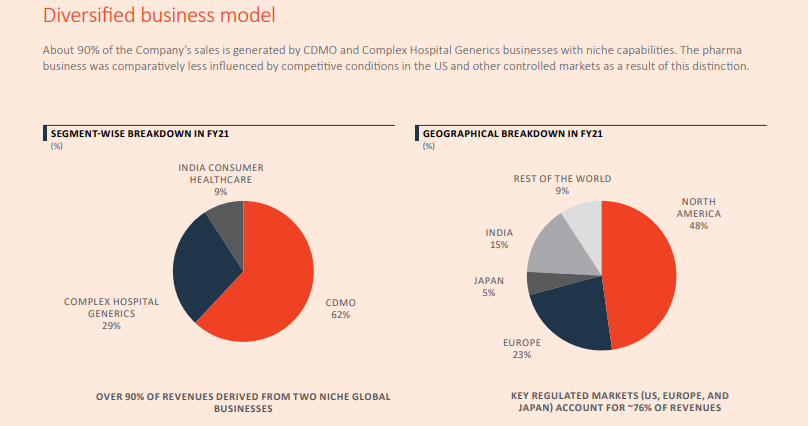

Piramal Pharma Limited (PPL), a subsidiary of Piramal Enterprises Limited, offers a portfolio of differentiated products and services through end-to-end manufacturing capabilities across 14 global facilities and a global distribution network in over 100 countries. PPL includes an integrated Contract Development and Manufacturing Organization (CDMO) business, Complex Hospital Generics business, and India Consumer Healthcare business, selling over-the-counter products in India.

Market Scenario: Pharma

The role of the pharmaceutical industry has become even more pronounced in the wake of the COVID-19 crisis. In these challenging and volatile times, pharmaceutical and healthcare companies play a vital role in facilitating the global supply of critical drugs while planning for new vaccines and therapeutics. This makes the Pharma industry one of the most critical and most resilient industries in such periods of uncertainty.

The pharmaceutical industry has also been impacted both on demand as well as supply side. Even though the impact on the demand side may be short-lived, that on the supply side is expected to have long-lasting effects on the global pharma supply chain.

Some governments restricted the export of certain pharmaceutical products at various times during the pandemic to concentrate limited supplies on domestic demand. When the pandemic was at its peak, the industry faced some difficulties, especially with regard to input materials being supplied from China.

On the demand side, pharma products are driven by underlying medical requirements, which are unlikely to change materially due to COVID-19. Any fluctuation observed in sales and procurement patterns are expected to last only in the short-term.

New opportunities also emerged for the pharma industry with increasing demand in certain categories such as hygiene products or preventive healthcare products and creation of essential redundancies in the supply chain by global companies. Enhanced focus on regional and local manufacturing is expected to boost new opportunities for companies with global production networks, a track record for reliable supply, and sound EHS (Environment, Health and Safety) practices. Most companies are likely to focus on operational resilience, agility, and transparency through greater deployment of digital and analytical tools and automation of processes.

Overall, the industry is undergoing unprecedented changes as the crisis passes. Key regulatory agencies are considering product sampling at borders, reviewing the company's compliance history, sharing information with other governments, and speedier approvals of regulatory submissions. Securing supply chain and ensuring business continuity while maintaining a strong focus on quality and compliance is the need of the hour. Pharma companies that are able to prepare for these changes with agility and set proactive controls and mechanisms should emerge stronger as the impact of pandemic subsides.

Complex Hospital Generics

Billion. Generic injectables represent ~20% of the US generic market. Capabilities in injectables are harder to acquire and cost heavy. Due to high entry barriers such as high initial investments for supplying and sustaining medical devices such as vaporizers, as well as dedicated production facilities for difficult-to-manufacture products, competition remains limited as compared to traditional generics. On an average, generic injectables have less than 4 market participants per product as against oral generics at 7 participants. Furthermore, a considerable portion of each of these categories is made up of institutional group purchasing organisations (GPOs) or tenderbased industry, both of which are extremely relationship-based and highly technical. These factors create hurdles for less-experienced competitors and new entrants. The high cost and operational burden of injectable capabilities increases the possibilities of long term contracts with customers and GPOs.

The Complex Hospital Generics business has a presence in inhalation anaesthesia, injectable anaesthesia and pain management, intrathecal therapy and other injectables. PEL is vertically backintegrated for inhalation anaesthesia and leverage relationships with a global network of partners for sterile injectables. The Company has a defensible and differentiated portfolio across these key hospitalfocused products and a strong pipeline of over 25 products across various stages of development.

PEL’s products are sold in over 100 countries in key markets including US, UK, Germany, France and Italy, and through highly committed distribution partners elsewhere. The Company caters to hospitals, surgical centres and veterinary centres with a workforce of over 400 employees globally.

PEL continues to strengthen its supply chain capabilities through vertical integration, cost effective and scalable infrastructure and strong relationships with developers and manufacturers. To improve the supply, it has been sourcing key starting materials (KSMs), APIs, and finished dosage forms from partners in multiple countries. The Company has consistently delivered high growth due to significant presence in specialised therapy areas and diverse hospital generics with high-entry barriers. Its continuous strategic acquisitions enhance the product portfolio by targeting products that are closer to commercial stages. PEL also plans to expand into the broader complex hospital generics space by identifying opportunities in new markets.

Complex Hospital Generics business revenues fell by 10% to ₹1,669 Crore during the year because of global decrease in surgeries and other hospitalisations. However, due to diversified product offering, PEL injectable pain products used in ICUs (Intensive Care Units) for treatment of Covid-19 patients and intrathecal portfolio performed well.

India Consumer Healthcare

The health-focused branded consumer segment in India has a market size of around US$ 19 billion. The consumer healthcare market is highly underpenetrated and the segment is expected to continue growing at a considerable rate in the years to come due to a young, urbanising population with increasing health consciousness, digital revolution, retail disruptions, and continued value-seeking behaviour of consumers. There is an upward swing in online shopping considering the visibility, targeted positioning and almost infinite shelf space offered by e-commerce platforms

PEL has built a diverse and extensive portfolio of 21 brands across categories including analgesics, skin care, VMS, kids’ wellness, digestives, women’s health, and hygiene and protection. Among its several successful brands, five major ones account for over 60% of the revenue. Many of its brands feature in the top 100 OTC brands in India. With a direct reach to over 250,000 outlets across India, the products are distributed by a field force of over 1,200 people.

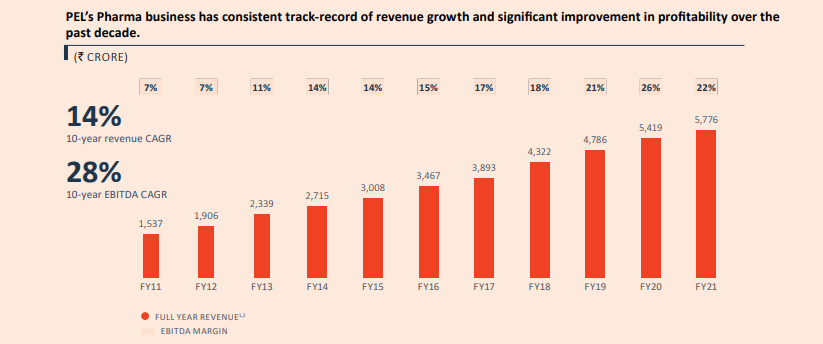

Revenue from Pharma business grew by 7% YoY in FY2021 to ₹ 5,776 Crore on account of high growth in CDMO and India Consumer Healthcare business, which was partly offset by lower performance in Complex Hospital Generics business. Revenue has grown at a CAGR of 14% over the last decade, now contributing 45% to overall PEL revenue mix. The Pharma business has delivered a strong growth in EBITDA margins from 7% in FY2011 to 22% in FY2021.

Fundraising in the Pharma business

To raise strategic growth capital for the Pharma business and as a step in the direction of eventual demerger and separate listing of the Pharma and Financial Services businesses, PEL decided to undertake a fund raise in its Pharma business. Accordingly, Pharma businesses of PEL were integrated into a subsidiary of PEL – Piramal Pharma Limited.

In October 2020, PPL received ₹3523.40 Crore on closure of the transaction for 20% equity investment from The Carlyle Group Inc. The transaction valued the Pharma Business at an enterprise value (EV) of US$2,775 million.

Financial Highlights

Financial Services

Income from the Financial Services business declined 8% YoY to Rs 7,033 in FY2021 as compared to Rs 7,649 Crore in the previous year. The YoY revenue decline was primarily due to the reduction in the wholesale loan book, in line with its stated strategy.

Healthcare, partly offset by a decline in Complex Hospital Generics due to demand volatility in the wake of COVID-19. Pharma revenues grew at a CAGR of 14% over the last ten years and contributed 45% to PEL’s overall consolidated revenues in FY2021.

Pharma

Revenues for the Pharma business increased by 7% YoY to Rs 5,776 Crore in FY2021 from Rs 5,419 Crore in FY2020. The increase was driven by strong growth in Pharma CDMO and India Consumer

Finance Costs

Finance costs for the year declined 21% YoY to Rs 4,209 Crore in FY2021 from Rs 5,321 Crore in FY2020, driven by a reduction in overall borrowings, as well as a decline in average cost of borrowings, particularly for the Financial Services business.

Depreciation and amortization

Depreciation and amortization expense for the year increased to Rs 561 Crore as compared to Rs 520 Crore in FY2020, primarily due to higher depreciation at Pharma overseas entities, on account of additions to plant & machinery, capitalization of intangible assets, and foreign exchange movements.

Taxation

Current Tax expenses were Rs 785 Crore in FY2021 vis-à-vis Rs 203 Crore in FY2020, due to a yoy increase in profit before taxes. However, both FY2021 and FY2020 were further impacted by onetime tax adjustments

Net Profit after Tax

Reported net profit after tax for FY2021 stood at Rs 1,413 Crore compared to Rs 21 Crore in FY2020, as the prior year was impacted by several one-time, non-recurring items including MAT credit reversal and incremental provision in the Financial Services business in response to COVID-19

Results for Q1 FY2022

August 6, 2021; Piramal Enterprises Limited announced its consolidated results for the First Quarter (Q1) FY2022 ended 30th June 2021. 3

P&L Performance

Q1 FY22 revenues of INR 2,909 Cr., broadly stable year over year

Q1 FY22 Net Profit at INR 534 Cr., increased 8% year over year

Balance Sheet

Equity increased by 29% to INR 34,996 Cr. since March 2019

50% reduction in Net Debt by INR 27,677 Cr. since March 2019

PEL Net Debt-to-Equity at 0.8x

DHFL Acquisition – Significant progress made in Q1 FY22

Resolution Plan received approval from NCLT and Monitoring Committee appointed in June 2021

Implementation of the Resolution Plan is in progress - To be completed within 90 days of NCLT approval, as per regulatory requirement

Ajay Piramal, Chairman, Piramal Enterprises Ltd. said, “Despite the impact of the second wave of Covid-19, Piramal Enterprises has delivered resilient performance during the quarter with Revenues at INR 2,909 Crores, Net Profit YoY growth by 8% to INR 534 Crores. The company continue to maintain a strong balance sheet, with net debt-to-equity ratio at 0.8x.

In Financial Services, its resolution plan for DHFL’s acquisition received NCLT-approval in June-2021. Piramal Enterprises is on track with the Monitoring Committee mandate for completion of this transaction within 90 days from NCLT approval. After successfully going through the recent consolidation phase, Piramal Enterprises is now transitioning from a wholesale-led to a well-diversified Financial Services business. The transition augmented by the DHFL acquisition will not only bring quantum growth in its loan book but also create a large India-wide platform that will enable it to deliver sustained growth and profitability in the years to come.

The company's Pharma business continues to deliver robust performance during the quarter, with 31% YoY revenue growth, indicating the strength of its business model. In addition, post the capital raise from the Carlyle Group, Piramal Enterprises has accelerated on its two-pronged strategic growth trajectory though investments in both organic and inorganic initiatives.

While the company remain cautiously optimistic for FY22, the company see a strong runway for growth across both its businesses. The company's immediate focus will be to effectively integrate DHFL with its Financial Services organization. Pursuant to which, the company will be better positioned to announce its plan to create two separate listed entities in Financial Services and Pharma.”